Join Puck to listen to this article

The early 2010s were an epic, perhaps unreasonably optimistic time for the direct-to-consumer business. Everlane, once seen as the next Gap, launched in 2011 with the promise of “radical” pricing transparency. By 2015, Warby Parker was in the process of turning a $2,500 seed investment from a Wharton venture initiative into a $1.2 billion valuation. Soon enough, everyone was pitching themselves as the Warby Parker of… well, something. It looked as if we’d never step inside a store or buy anything indirectly again. That same year, Away was founded to upend the luggage business.

Of course, it didn’t quite work out that way. And 10 years later, those early D.T.C. darlings have taken radically different paths. Warby Parker’s business grew and grew before inevitably flattening out: The company’s market cap has declined from nearly $7 billion at its I.P.O. four years ago to $2.5 billion now. (Lets see if its partnership with Google can erase those losses.) Away, whose executives I recently interviewed, is looking to redifferentiate the brand after a pandemic slump and amid growing competition. Meanwhile, Everlane, which reportedly did around $200 million in retail revenue in 2023, feels rudderless. Their recently launched “clean luxury” campaign has done little, so far, to mitigate the brand’s midlife identity crisis. It all has a whiff of Selina Meyer’s “Continuity With Change” slogan on Veep.

Indeed, Everlane’s woes are representative of an entire generation of faded D.T.C. darlings, all of which promised to revolutionize retail by delivering the same products for less by eliminating middlemen and pass-through fees. But those early D.T.C.s didn’t account for rising customer acquisition costs, or the traffic advantage of multibrand retailers, both digital and in-store. Meanwhile, they all raised money inexpensively, largely spent fecklessly, and buckled under the weight of their respective capital structures. V.C.s like Forerunner, L Catterton, and NEA poured millions into these brands, creating valuations that made profitable exits nearly impossible.

Bonobos has served as a cautionary tale of what happens when venture growth pressure meets retail reality: The company was acquired by Walmart in 2017 for $310 million, and was sold two years ago to WHP Global for $75 million. And that’s one of the better outcomes, actually. So how are the O.G. D.T.C.s faring about a decade after the revolution? Herewith…

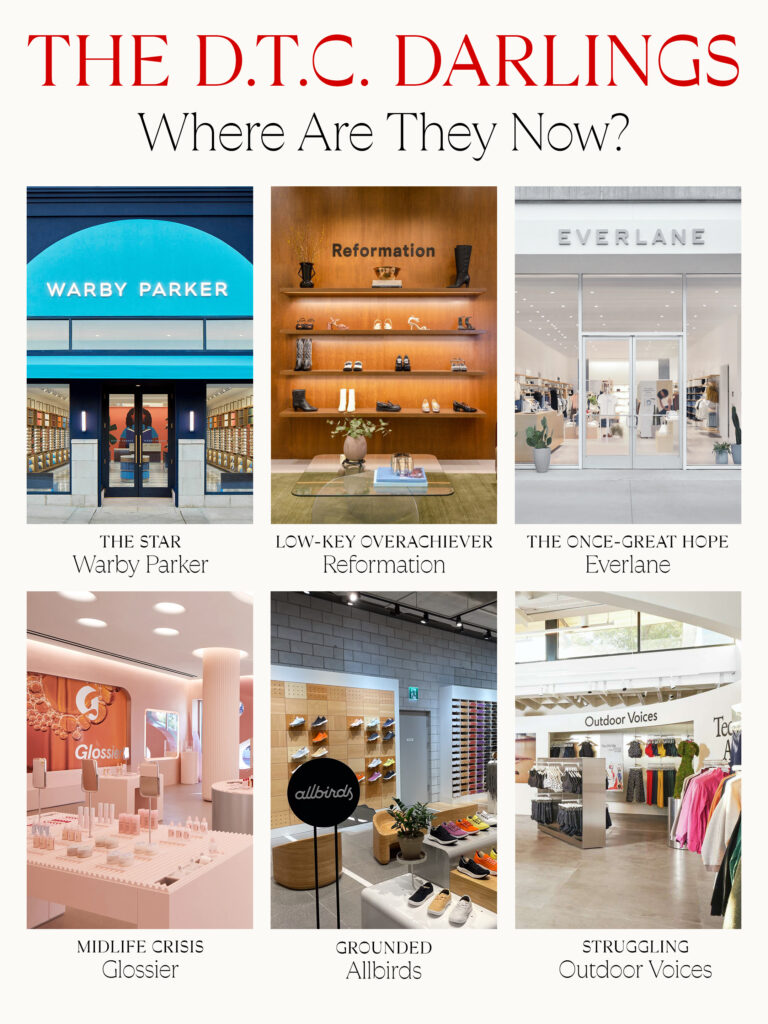

The Star: Warby Parker

Anomalously, Warby co-founders and co-C.E.O.s Neil Blumenthal and Dave Gilboa are still leading the company they founded 15 years ago, and the new Google partnership shows they’re still interested in innovating beyond just selling frames. Their stock is down almost 60 percent from its 2021 peak, but it still feels like they’ll be an inevitable part of eyewear, whether it’s prescription glasses or Google’s A.R. glasses. They’ve grown to 276 stores, added Target partnerships, and launched an optometrist program to keep glasses literally in front of customers’ eyes, even if they’re no longer enjoying the disruptor halo and saving bespectacled consumers from EssilorLuxottica’s monopolistic pricing. Warby closed out 2024 with over $770 million in revenue, up 15 percent year-over-year.

The Overachiever: Reformation

After 16 years in business and just $37 million in capital raised to date, the brand has stayed relevant through smart marketing and styling that adapted to changing trends. (They also set some trends of their own.) The company also weathered hot-and-cold consumer interest over the years. In 2018, Reformation launched in 20 Nordstrom stores—the same store count that both Rothy’s and Dôen recently launched with. The brand, which was doing more than $350 million in 2023, has said it’s profitable and currently on track to exceed $500 million in annual sales.

The Once-Great Hope: Everlane

The brand that was once seen as the next Gap and planned to scale to $1 billion in revenue is way off that trajectory. Plagued by C.E.O. and designer turnover, and working to settle into their latest messaging pivot to clean luxury, Everlane is currently bringing in much closer to $200 million–$225 million. The brand, which has great basics (but so does everyone), seems to be moving toward Aritzia-inspired looks (similar to this tank) as it puts an investment from L Catterton to work.

The Cautionary Tales: Glossier, Outdoor Voices & Allbirds

Glossier, the quintessential Millennial beauty brand, raised more than $260 million with no potential suitors and a murky path to an I.P.O. And, as my Puck partner Rachel Strugatz reported last week, Rhode’s recent acquisition makes Glossier’s future even fuzzier. I was surprised recently to see that the top Glossier searches, according to Google Trends, are actually for merch and P.R. kits—not the actual products they need to sell. “Glossier cherry lock” from their Cherry Balm Dotcom launch, and “glossier laptop mirror”—both giveaways you can find on the resale market—are leading searches for the brand. Never a good sign…

Of course, Glossier looks like a veritable unicorn next to some of its generational peers. Outdoor Voices, which was once the most exciting new player in the nascent athleisure space, was quickly overtaken by Alo, Set Active, and Beyond Yoga as O.V. descended into leadership turmoil—and eventually ousted its founder. The top search regarding Outdoor Voices has been, “Where to buy Outdoor Voices in person.”

And then there’s Allbirds, the online shoe company for I.T. guys and people without taste that managed to go public in 2021—mainly because investors wanted their money out—and then immediately stumbled. Allbirds, which briefly touched a $4 billion valuation on the day of its I.P.O., now has a market cap of around $60 million, a 99 percent decline. As I noted in my recent piece about Rothy’s, Allbirds took too long to innovate beyond their single knit style.

The Next 10 Years

It’s worth noting that all of these brands, even the ones that didn’t make it, probably could have thrived as lifestyle businesses with smaller funding rounds and sustainable growth. Venture capital changed their DNA, and so did inexperienced and often avaricious management teams who deluded themselves into believing they were running tech companies just because they sold goods over the web. And yet, the brands that we talk about today—Staud, Dôen, Toteme—all benefited from their mistakes. In many cases, they learned to prioritize direct sales with multiple stores, something unthinkable without these original pioneers. The winning formula du jour is a mix of wholesale and direct. But that’ll probably change soon, too.