While the big money has returned, auction houses are reducing estimates for cheaper works to entice buyers and minimize their losses. Now, the latest data reveals a big shift is taking place in the middle market, too.

Inner Circle Exclusive

Auctioneer Yü-Ge Wang sells Gerhard Richter's “Kerze (Candle)” at Christie's auction.

Photo: Courtesy of Christie's

There was hope that the success of the all-important May sales in New York would loosen purse strings and usher in a new spirit of acquisitiveness for art collectors. From my conversations with dealers, however, those hopes were misplaced, or will at least require patience. It remains as hard as ever to get works sold, although many dealers tell me they’re making bigger deals… when they’re able to make them.

I thought of these conversations while going through the numbers from the May auctions—especially the data from the bidding quintiles, which show that the auction houses have greatly reduced estimates, particularly in the lower registers. The result has been a minimization of losses in the average premium price and their confinement to the very bottom of the market. The downshift in estimates from November 2025 to May 2026 was even greater, but the same logic holds: Reductions in estimates have helped reduce the drop in average premium prices.

This suggests that, at the moment, the auction market is more responsive to buyers’ price expectations than the private market; the auction houses are offering bargains, and buyers are snapping them up. Also, what’s interesting about the data below is that, as the top of the market revives, a big shift seems to be taking place in the middle market.

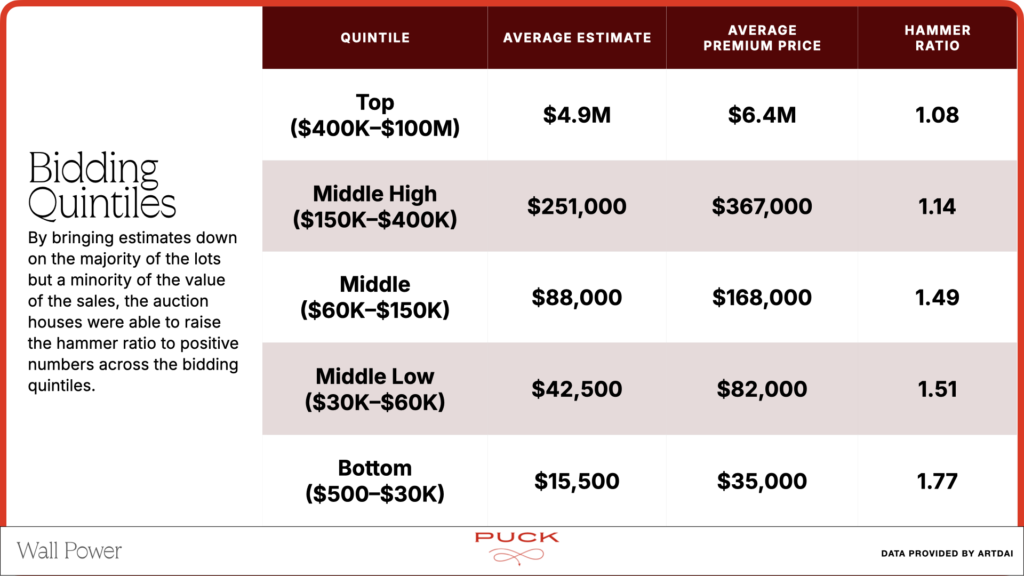

Five-Tier Revelations

Every major auction season, I create a chart of the bidding quintiles, ranking all of the lots offered by their presale estimates, high to low, then sorting them into five groups. The quintiles reveal the composition of each market sector, including the estimate range, average estimate, average premium prices of sold works, and overall hammer ratio. (As you know, the hammer ratio is the aggregate hammer price of all sold lots in the quintile divided by the aggregate estimates for all lots offered in the quintile.) The all-important hammer ratios measure the strength of bidding.

Obviously, the art market isn’t a monolith. Strength at the top can mask weakness at the bottom or obscure what’s happening in the middle. You get the point. But looking at the changes in the quintiles over time—especially a volatile period like the past three seasons—is almost always revealing.

Consignors have finally come to understand that the overall estimate level for art has been too high. You can see that in the general shape of the market: Bidding is strongest for the lowest-priced works and gradually softens as you go up the quintiles. As we saw in the numbers two weeks ago, the overall hammer ratio rose into positive territory in the May sales, at 1.10. But the top of the market—works estimated between $400,000 and $100 million—was slightly weaker, at 1.08.

Compare that to May 2025, when the overall sales had a disappointing 0.89 hammer ratio, with the top quintile coming in at 0.87. In November, this sector of the market had gotten noticeably stronger, with a hammer ratio of 1.10 that mirrored the overall hammer ratio. The top quintile in November 2025 was also colored by the sales of Leonard Lauder’s Klimts; the overperformance of the top Klimt greatly added to the hammer ratio.

This May, the average estimate of a work in the top quintile ($4.9 million) and average premium price ($6.4 million) were the same as last November. But in May 2025, the average estimate in the top quintile was $3.3 million and the average premium price was $3.5 million. These numbers show the turnaround happening at the top.

That matters: In many ways, this top quintile is the art market, since it skews so heavily toward the high-value works that represent most of the total value. (In the May sales, for example, it accounted for 90 percent.) But that doesn’t mean the other quintiles don’t matter. As I’ve said numerous times during the art market slump of the past three years, the health of the market can be seen in the demand for lower-value works and the volume of sales. Cultural property is clearly very important. The only question is how it gets distributed.

That brings us to the other important observation from the bidding quintiles. This May, the average estimate for each of the lower four quintiles and the average premium price (hammer price plus fees) were lower than in the previous two seasons. For the middle-high quintile, the average estimate and average premium price were $251,000 and $367,000, respectively. Last year they were $335,000 and $388,000, and in November they were $402,000 and $522,000. The downgrades were consistent throughout the quintiles. The middle-low quintile saw $42,500 and $82,000 as the average estimate and average premium price; a year earlier, they were $50,000 and $82,000. In the fall, they were $68,000 and $104,000.

When Estimates Attract

It seems logical that lower estimates would attract greater bidding, which is why we’ve seen the hammer ratios rise. But what accounts for the overall drop in estimates and selling prices for the 10 percent of the market value represented by the lower 80 percent of lots? One thought is that the wholesale downgrade in pricing is the result of the shift in property from artists currently practicing to historical material. With fewer recent auction records, the historic property tends to get estimated lower.

The weakness in that theory, however, is that we’ve been seeing a turn toward historical works for several seasons. Why would the average estimates and prices for lots in all of the quintiles rise from May to November 2025, only to fall in May 2026, if the pricing were a result of the changing mix of property from young artists to old stuff?

We’ve heard from auction house specialists and heads of sales that they’ve been actively encouraging consignors to accept lower estimates. It appears the consignors have listened. Across the lower four quintiles, average estimates fell, even as they held firm from November to May in the top quintile. In the middle-high and middle quintiles, the average premium price also fell, but at a much lower rate than the estimates. And in the lower two quintiles, cutting estimates either helped maintain the average premium price or boosted it. The average estimate for a work in the middle-low quintile was $50,000 in May 2025. It dropped to $42,500 this past season, while the average premium price remained at $82,000.

In the bottom quintile, the average estimate for a lot in May 2025 was $18,000, and the average premium price was $30,000. A year later, the average estimate was slightly lower, at $15,500, but the average selling price was 16 percent higher, at $35,000. Those numbers validate the conventional wisdom that lower auction estimates generate more competition and, thus, higher prices.

Shared with you by a Puck member

Enjoy this free article thanks to a friend. You can keep exploring Puck with a free account or enjoy a 14 day free trial.

Didn't get an email? Check your spam folder and confirm the spelling of your email, and try again. If you continue to have trouble, reach out to fritz@puck.news.

Didn't get an email? Check your spam folder and confirm the spelling of your email, and try again. If you continue to have trouble, reach out to fritz@puck.news.

Member Exclusive

Get access to this story

Create a free account to preview Puck’s full offering, including exclusive articles, private emails from authors, and more.