Netflix’s shock exit from the Warner Bros. Discovery sweepstakes likely gives Paramount the victory, saddling them with a mountain of debt, and a slightly smaller mountain of unanswered questions. Why did Ted & Co. walk away so abruptly? Can Paramount get this thing through regulators? And exactly how many people are about to get fired?

Barring intervention from regulators in this country or overseas, the move clears the way for David Ellison and the $111 billion he and his father cobbled together to take over Warner Bros., HBO Max, CNN, and all the other cable networks.

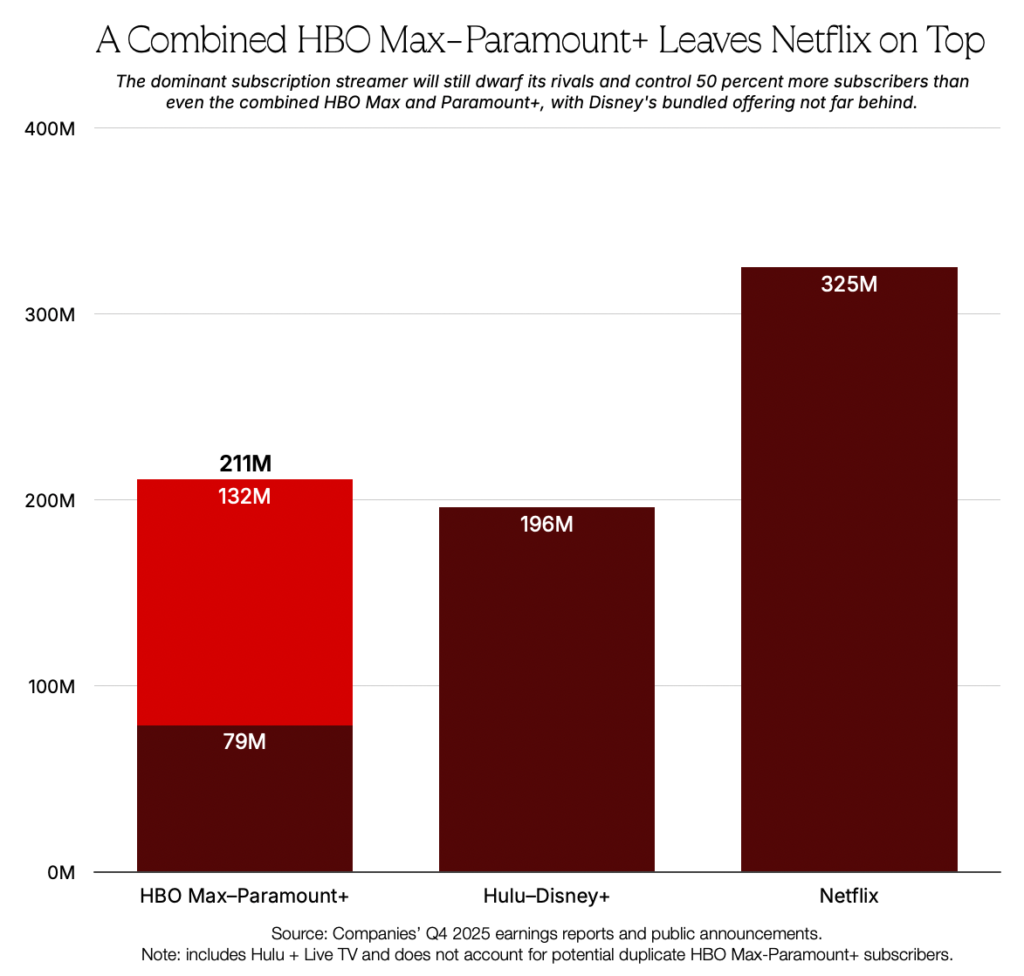

Photo: Anna Moneymaker/Getty Images

Whew! What a whirlwind week. Once Paramount finally agreed to raise its offer for Warner Bros. Discovery to $31 per share and boost a bunch of incentives, I think most people in town thought Netflix would at least go one round of matching. But no, co-C.E.O.s Ted Sarandos and Greg Peters folded this afternoon, right after Sarandos met with Attorney General Pam Bondi in D.C. Barring intervention from regulators in this country or overseas, the move clears the way for DavidEllison and the $111 billion he and his father cobbled together to take over Warner Bros., HBO Max, CNN, and all the other cable networks.

A million thoughts and questions come to mind, and people throughout Hollywood and the news business are scared and confused. So I asked Bill Cohan, Puck’s Wall Street maven and the author of Dry Powder, to open a Google doc and discuss it all in the immediate wake of the announcement. Here goes…

“Nice to Have” vs. “Need to Have”

Matt: Bill, first off, congrats. You urged Ted yesterday to walk away, and today he does. I always thought Paramount would win in the end because they need Warners (or at least the Ellisons feel they need Warners) to effectuate their big media-tech makeover/roll-up strategy, and David seems to have something to prove here to Larry. But Ted, by contrast, always said Netflix didn’t need to do this.

Bill: No, it was nice to have vs. need to have, and Ted’s shareholders clearly didn’t like this deal. He absolutely did the right thing by walking away. He showed both that he could do a big deal—he had a merger agreement with WBD, after all—and be a disciplined buyer when the cost got way out of control. Netflix’s share price was down about 35 percent since the deal noise first started, that’s more than $150 billion in lost value. It shot up tonight in after-hours trading once Ted walked.

Matt: I thought it was strange that Netflix didn’t even take the four allotted days to decide whether to match Paramount. But as MoffettNathanson noted tonight, decisively ending the pursuit sends a message of strength and confidence in its core business at a time when shareholders were questioning whether the pursuit of Warners meant Netflix was worried about growth.

Bill: That’s right. As for the Ellisons, they don’t care what the Paramount stock price does in the short term. It’s a controlled company, owned by the Ellisons, with others along for the ride. All they cared about, it’s clear, is that they won WBD, and now they have.

Matt: It’s nice to be rich.

Bill: How are people around Hollywood taking this news?

Matt: It’s a gut punch for a lot of people. I’ve said from the beginning that there is no good outcome here for Hollywood. As much as Netflix was a dominant player buying up a competitor, Paramount, by its own admission, is planning $6 billion in cost savings, which means historic layoffs. Netflix claimed Paramount will require $16 billion in cuts to make this math work.

Bill: We’ll get to the financials in a second.

Matt: Warners has changed hands nine times since it became an independent movie studio in 1923. Now it’ll likely be another year or two of grim town halls (Warners C.E.O. David Zaslav scheduled one for tomorrow) followed by H.R. meetings and thousands of employee emails getting immediately shut off. The CNN people, who certainly didn’t love that their new owner was thumbs-upping with Lindsey Graham on Tuesday night, are freaking out about being combined with CBS News and Bari Weiss potentially taking over. (“Anderson can’t get away from her!” one CNNer texted.) The HBO Max people are worried about diminished output and that Casey Bloys and his team might bail rather than report to Cindy Holland at Paramount. And the movie people have serious suspicions about the plans for Mike De Luca,Pam Abdy,and all the filmmakers at Warner Bros.

Ellison has promised 30 movies a year in theaters between WB and Paramount, but few believe that is a long-term strategy. No reason, other than the example of every other merger in Hollywood history, including Disney and Fox in 2019. Then there’s the whole question of what happens to the combined platforms and subscriber bases of Paramount+ and HBO Max. Does one go away? A bundle? Not to mention Ellison’s Saudi and Middle East backers. After much initial disgust, I think people in town were getting used to the idea of Netflix winning this deal. Netflix is at least a proven, professionally managed, and highly successful entertainment company. Sarandos had assuaged some fears by committing to theatrical releases and keeping the studio independent. And then in the course of two days it all changed. One top WBD exec told me the mood in his unit is bleak.

Bill:It was going to be a rough ride for the WBD folks no matter who prevailed, but I do believe that Netflix would have left things alone that weren’t broken. Paramount has a very different agenda. The Ellisons would be wise not to mess with too much, but I’m sure they won’t be able to resist, and the financial underpinnings of this deal will require certain actions, just like when Discovery took over WarnerMedia. So pour one out for Hollywood tonight.

The Politics

Matt: Let’s discuss why Paramount won. Obviously this deal got very expensive. The Ellisons were floating $19 a share in their first offer, and they closed at $31, plus a bunch of sweeteners.

Bill: Don’t forget that the WBD stock got as low as $7 a share. So $7 to $31 a share is pretty impressive. Zaz gets the Dealmaker of the Year award.

Matt: That’ll earn him some high-fives at his breakfasts with Barry Diller and David Geffen, but he should expect to get the cold shoulder from the creatives he has so desperately coveted in L.A. Margot Robbie! Remember me? I’m the guy who bolted my failing cable TV company onto Warner Bros., then sold the studio out of existence and pocketed hundreds of millions of dollars for myself. Margot? Margot???

Bill: He also got Larry Ellison to cave on every significant deal point, to be honest—something I’m sure Larry Ellison rarely does. When he bought up Manalapan, Florida, I’m sure he was the one in control.

But Zaz got him to pay the $2.8 billion break-up fee to Netflix; to agree to a $7 billion fee if the regulators stop the Paramount–Warners deal; to let him refinance a $15 billion bridge loan and to pay a $1.5 billion fee related to Warners’ exchange offer last summer. And my favorite give: in addition to convincing Larry to put up the equity, Zaz got him to agree to put up more equity if his bankers start making noises about walking away from the deal at closing. That was the real coup for Zaz, and it probably went a long way toward getting the WBD board to switch its allegiance to Paramount. The “ticking fee” was just icing on the cake.

For an ex-M&A guy like me, this is the deal of the century. Books will be written about it. (Usual disclosure: Due to a recent transaction, Zaz is a de minimis investor in Puck; RedBird Capital, the Ellisons’ financial partner in Paramount, is a minority shareholder.)

Matt: But there were so many other non-financial factors. Ted kept insisting this was “not a political deal,” yet he found himself cozying up to Trump people in D.C. again today in what basically became a Super Bowl of shamelessness between Sarandos and Ellison. The bottom line is that Trump likes what he sees so far from Paramount. And on the contrary, Republican attorneys general were vowing a long fight against Netflix over “wokeness,” or whatever. Trump himself demanded Netflix boot Susan Rice from the board, which Ted was never gonna do.

Do you think the path to closing is really so much easier for Paramount that it ultimately scared Netflix off, or is it now just a different set of regulators who are gonna give Paramount a hard time? After all, ParBros (WarnerMount?) is clearly a “horizontal” merger of two competitors. Rob Bonta, California’s A.G., announced tonight that it “is not a done deal,” and that “we intend to be vigorous in our review.”

Bill: Well, as we all heard ad nauseam just last week, Paramount believes its deal for WBD already has the approval of the Justice Department. But the D.O.J. could take another look now that it has won. (Pam Bondi probably won’t, but she could.)

So, let’s assume the D.O.J. has approved. The company still has to get through the E.U. regulators, who love to give big, brassy American mergers a tough time. The Paramount crew thinks they are cool in the E.U. too, but we shall see. Elizabeth Warren and Cory Booker can make all the noise they want. But guess what? U.S. senators have no say in approving a merger, so it’ll just be noise, as we saw at that Senate hearing a couple of weeks ago. That’s when Ted, by the way, must have figured les jeux sont faits.

The L.B.O. Math

Matt: Okay, so walk me through this winning bid and the potential red flags for the combined company. Sarandos kept referring to the Paramount deal as the largest leveraged buyout in history. That sounds dangerous.

Bill: Well, this is going to be one leveraged puppy. According to the just-released Paramount Skydance 10-K, the company has a little more than $10 billion of net debt already, and had around $3 billion of adjusted EBITDA in 2025 (a measure of profits), so leverage of around 3.3x. Not terrible. Not great. Now, with this $111 billion acquisition of all of WBD, Paramount will be adding something like another nearly $60billion of debt to the equation, from three big Wall Street firms: Bank of America, Citigroup, and Apollo. So, let’s call it $70 billion of net debt, maybe more maybe less, on something like $12-or-so billion of adjusted EBITDA from the combined company.

Paramount is projecting $3.8 billion of adjusted EBITDA for 2026 and let’s say WBD will achieve the balance, earning around $8.7 billion of adjusted EBITDA this year. (Both are just estimates, of course). That’s nearly 6x leverage, and we’re talking about a huge amount of debt. In 2025, WBD hit that $8.7 billion in adjusted EBITDA exactly, a 3 percent decrease from the previous year, which doesn’t exactly sound like a growth business. The tougher news was that the just-completed fourth quarter was more of a struggle, with an adjusted EBITDA of $2.2 billion, a 20 percent year-over-year decline, with most of that decline coming from linear TV channels. That, of course, will be going into Paramount’s column when the deal closes.

By the way, the numbers are still moving all around, and I’m writing this before Paramount has released the final figures for the debt and equity. Netflix predicted Paramount would have $84 billion of pro forma debt and 7x 2026 pro forma EBITDA. We will update the numbers when we know more…

Matt: Yikes. Wasn’t a debt overload by Zaslav and the Discovery people the exact reason the combined Warner Bros. Discovery never achieved sustainability and ended up having to be sold? The fundamental problem with these companies is the melting ice cube of linear television. And now Ellison is taking that melting Paramount TV business and doubling down on a bunch more TV networks, like TNT, Cartoon Network, and TBS, that don’t have much of a future. There are synergies, of course, but overall it’s a no-future business.

Bill: Well, Warners did not have to be sold. Zaz and his board decided to put the company up for sale after the Ellisons made a number of unsolicited bids and Zaz heard from Netflix and Comcast, too. I think WBD would have been happy splitting the company into two pieces—now C.F.O. Gunnar Wiedenfels won’t be a C.E.O., or at least not yet—but decided ultimately to sell the company to the highest bidder. Give Zaz and his board credit.

On the other hand, the Ellisons and their partners are investing a huge amount of equity, too—something along the lines of $45 billion. This is one of the largest L.B.O.s in history, but it’s more interesting than that because it will also remain a public company—so it’s more like a leveraged recap of sorts, with a huge pile of new debt and equity. What’s more, Ellison has pledged to put more equity in at closing if the debt providers start to balk because of questions about the solvency of this thing. So the deal will close, unless the regulators block it. And if they do, the Ellisons will owe Warners $7 billion.

Matt: Yes, it’s too bad for Gunnar, who would have been C.E.O. of the spun-off “stub” collection of TV networks. Didn’t work out for him.

Bill: Gunnar should be just fine with the roughly $145 million he stands to make from this deal. It’s not the $600 million Zaz may get, but he won’t go hungry.

Matt: It’s all kinda disgusting. But while this is personally embarrassing for Sarandos, Netflix can make a lot of shows and movies with the $2.8 billion breakup fee. If I were Ted, I’d use that money to go after CBS’s football package when the NFL opens up those deals soon. Or, as our colleague Eriq Gardnersuggested, start a 24/7 news vertical on Netflix and just hire away all the great talent from 60 Minutes and CNN. I’m also guessing it takes Ted about a week to go back to saying movie theaters are outmoded and dying.

Bill: Ha. Aside from Zaz, I think Ted is a big winner here. His stock price is already zooming back up, he gets the $2.8 billion, and he probably gets a big fat content deal with the combined Paramount/WBD. And he looks like a disciplined, clever dealmaker. He got the Ellisons to pay $31 a share! Let’s hope WBD doesn’t prove to be a poisoned chalice, as it was for AOL… and for AT&T. As I wrote on Wednesday, I wouldn’t be surprised if Ted, or someone else, doesn’t get the chance to buy Warners again sometime soon.

Matt: Oh god, it never ends.

Shared with you by a Puck member

Enjoy this free article thanks to a friend. You can keep exploring Puck with a free account or enjoy a 14 day free trial.

Didn't get an email? Check your spam folder and confirm the spelling of your email, and try again. If you continue to have trouble, reach out to fritz@puck.news.

Didn't get an email? Check your spam folder and confirm the spelling of your email, and try again. If you continue to have trouble, reach out to fritz@puck.news.

Member Exclusive

Get access to this story

Create a free account to preview Puck’s full offering, including exclusive articles, private emails from authors, and more.