{{ 'now' | timezone: 'America/New_York' | date: '%b %d, %Y' }} |

|

|

|

Greetings from Los Angeles, and welcome back to In the Room. Did you hear that Rob Bonta

wants David Ellison to sell CNN? Our partner Matt Belloni reports

that the California A.G. may push for a divestiture of the news network in exchange for forgoing a lawsuit. David would never agree to it, per my sources: He wants the network’s influence and its profits, and the CNN–CBS News tie-up opens up massive savings opportunities. But it is another headache, and Bonta has some leverage. Recall, according to the Journal, that Larry Ellison

reportedly told Trump that he and his son could overhaul CNN after the merger. (Paramount maintains no such commitment was made.)

On a related note, we hear that The New York Times is set to publish a story about how David is weighing Bari

Weiss’s future role at CNN, the need to bring in an experienced executive, and the broader anxieties at Hudson Yards in anticipation of the merger. I’ve written this story at least 20 times already (yeah, I know…), but I’m excited to see what fresh color they have to add! Meanwhile, I hear that David and Jake Tapper recently had dinner together here in Los Angeles.

As I’ve been saying for some time, this merger is already well underway!

In tonight’s email, my partner Julia Alexander takes a deep dive into the state of the paid newsletter business, and a massive new report from Tyler Denk’s Beehiiv on what’s driving influence in the industry. The findings here—and Julia’s insights on them—are invaluable for everyone in the space. And there are charts!

🎙️ Plus, on that latest episode of The Grill

Room, Julia and I dissected The New York Times’s sprawling exposé on former Athletic reporter Dianna Russini, what it really means to be an “insider” versus a reporter, and how the Times balances standards and ethics as it grows its business, courts new audiences, and elevates its own stars. Follow The Grill Room on Apple,

Spotify, or wherever you prefer to listen.

Also mentioned in this issue: Neal Mohan, Ted Sarandos, Greg Peters, Daniel Ek, Adam Mosseri, Austin Rief,

Azeem Azhar, Casey Newton, Charlotte Maines, Emily Sundberg, John Fulton, Kevin Roose, Larry Sanger, Lenny Rachitsky, Mark Rober, Matt Strauss, Nick Thompson, and more.

And finally, rest in peace to

Om Malik, the early internet entrepreneur, writer, and investor who inspired many of the era’s leading tech journalists.

Take it away, Julia… |

|

|

|

| Julia Alexander

|

|

- A Wikipedia

micro-scandal: Earlier this week, Wikipedia’s top editors instituted a rare sitewide ban on Larry Sanger, the company’s own estranged co-founder. Wikipedia is one of the last great collectivist projects on the web—maintained by a massive volunteer army that makes some 300,000 updates every day. On the face of it, Sanger was allegedly banned for inciting his nearly 100,000 followers on X to attempt to sway internal policy discussions within Wikipedia that could alter the

makeup of the site. But critics are already decrying that the decision had political undertones: For years, Sanger has been criticizing the site for alleged left-wing bias—a claim that the New York Post was all too happy to highlight in its reporting of the situation.

Trivial internet drama, maybe, but Wikipedia is still the seventh-largest site on the web—and the controversy is especially pertinent now that L.L.M.s are training themselves on its gargantuan repository of human

knowledge. Whatever bias is embedded in Wikipedia is also feeding ChatGPT and Claude and just about every chatbot. Elon Musk’s Grokipedia, which he launched last year, won’t be the last attempt to create a competitor. - Netflix isn’t chill: The streaming giant doesn’t report earnings for another three weeks, but analysts are already clenching based on Netflix’s previous soft forward-looking guidance. The company’s stock slumped to its

lowest in a year earlier this week, after Fox acquired Roku, prompting new questions about where Netflix will find more growth—even as nearly everyone agrees that it’s still the GOAT.

But what’s really keeping investors up at night are those engagement numbers—the key metric as Netflix moves to capture a larger share of the advertising business. Ad-supported tiers now make up the majority of all U.S. streaming subscriptions across all major platforms, according to a recent report from

Antenna, and engagement is crucial to negotiating the best rates. Plus, engagement is the core metric that Netflix’s teams use to try and determine average churn rate. Though Netflix is still the industry leader with a 2 percent churn rate (two percentage points lower than the average), any new concerns about declining engagement could spook Wall Street.

So what’s next? On next month’s earnings call, look for investors and analysts to ask Netflix executives hard questions about what’s

beyond TV shows and movies. Should co-C.E.O.s Ted Sarandos and Greg Peters follow NBCU’s Matt Strauss and invest in microdramas and vertical video? Should they expand their podcast partnership with Spotify’s Daniel Ek? Will they seek out more Mark Rober/Ms. Rachel–style YouTube deals? Should they have bought Roku? We’ll get some of these answers in a few weeks. - The YouTube creator gold rush, cont’d: One week after I suggested that Fox could use its Roku acquisition to get more of its Red Seat Ventures podcast stars into 90 million new U.S. homes, Amazon and Samsung have announced something very similar: partnerships with YouTube and Instagram, respectively, to bring mobile video to TV screens.

Amazon’s “Creator Hub” for Fire TV will prominently spotlight hundreds of YouTube creators on its home screen—the new TV Guide for

audiences. As Fire TV’s Charlotte Maines told a group downing rosé at Cannes Lions this week, Amazon is currently working with some 200 creators, with the goal to reach more than 500 by next year. Meanwhile, Samsung is teaming up with Instagram for a similar longform video experience on its smart TVs. (Kudos to Instagram chief Adam Mosseri for what I can only imagine was feigned excitement after the utter failure of Facebook Watch. If at first you don’t

succeed…)

Of course, no one benefits more from this activity than Neal Mohan and YouTube. But here’s a fun question to ponder: If Instagram is moving more into longform content, and YouTube is moving even more into Shorts, at what point do these platforms lose their differentiation?

|

|

|

|

And now, the main event... |

|

|

|

As the business matures, newsletter creators need new strategies—including more

differentiated content, smarter pricing, and community engagement—to stand out amid the glut. A new report reveals some crucial insights. |

|

|

|

For such a simple technology, email can be a tricky business. Newsletter companies like Substack and Beehiiv

now boast hundreds of thousands of independent publishers, a small portion of whom are making real money—generating eight-figure revenue for their host platforms in the process. Growth is impressive—Beehiiv recently said its paid subscriptions surpassed $19 million in 2025, up nearly 140 percent year over year—but slowing, especially on Substack, amid market saturation and inbox fatigue.

Indeed, the industry appears to be at an inflection point: It’s never been easier to start a

newsletter, or for an established media business to launch one, but how much can the market stand? And, perhaps more importantly in the A.I. era, how can independent operators stand out from the crowd?

Earlier this week, Beehiiv co-founder Tyler Denk and his team published a massive report on the state of paid newsletters in 2026, providing some

intriguing insights into what’s working, and not working, for media creators. Yes, this is Beehiiv’s own first-party data, meaning that trends may be different across Substack, Patreon, and elsewhere, but the team’s analysis is still relevant and applicable to anyone starting or growing a newsletter business. Naturally, I read the whole thing so you don’t have to. Here are three recommendations: |

1. You’re

Probably Underpricing

|

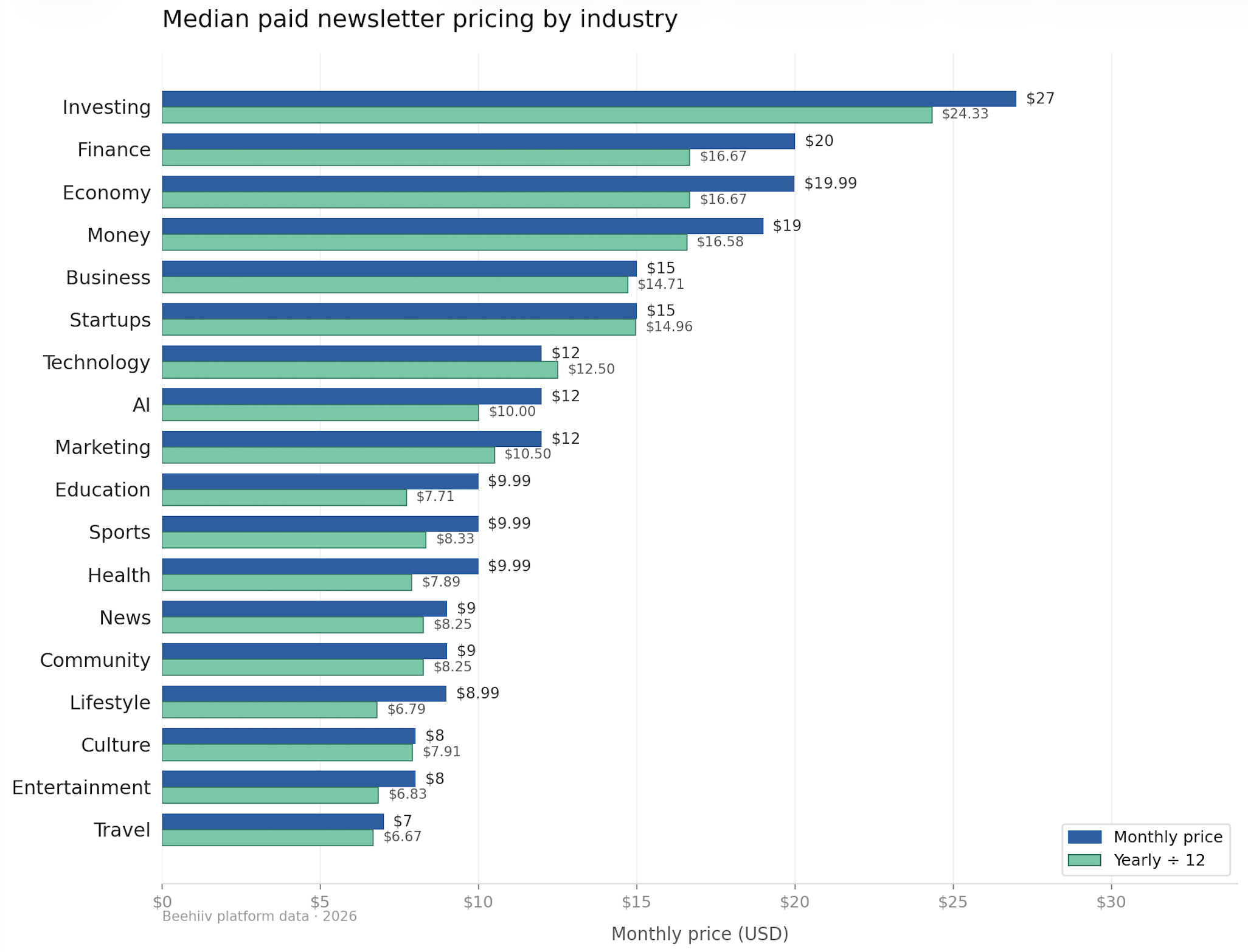

The median monthly newsletter subscription fee on Beehiiv is $10, a figure that hasn’t changed since 2024,

per Beehiiv. But that’s just the mass-market price. More professionalized and prosumer offerings are typically able to charge significantly higher rates. For example, financial-investing newsletters across Beehiiv charge a median monthly rate of $27. (Some of the most successful finance newsletters on Substack charge far more: Citrini Research, the platform’s top-ranked email product, charges $125 a month.) |

Even though investing newsletters have some of the highest churn rates (about 12 percent, compared to food

newsletters, which boast about 5 percent monthly churn), the lifetime value of the customer is much higher. Niche and B2B newsletter topics, the category that finance and investing often fall into, don’t need to charge mass-market prices because they’re professional service products.

Since mass-market newsletters are more likely to contain commoditized information that can be found on other websites, it’s easier to scale them up front but harder to retain an audience in the long run. It’s

the same lessons from the early digital media age, when mass-market content drove large audiences, which translated to strong advertising revenue. But a failure to invest in premium products with strong community ties, like newsletters, left these inflated and unessential brands at the mercy of social algorithms—and totally exposed with the advent of A.I. search. |

2. Hot Topics Don’t Always Make for Hot

Newsletters

|

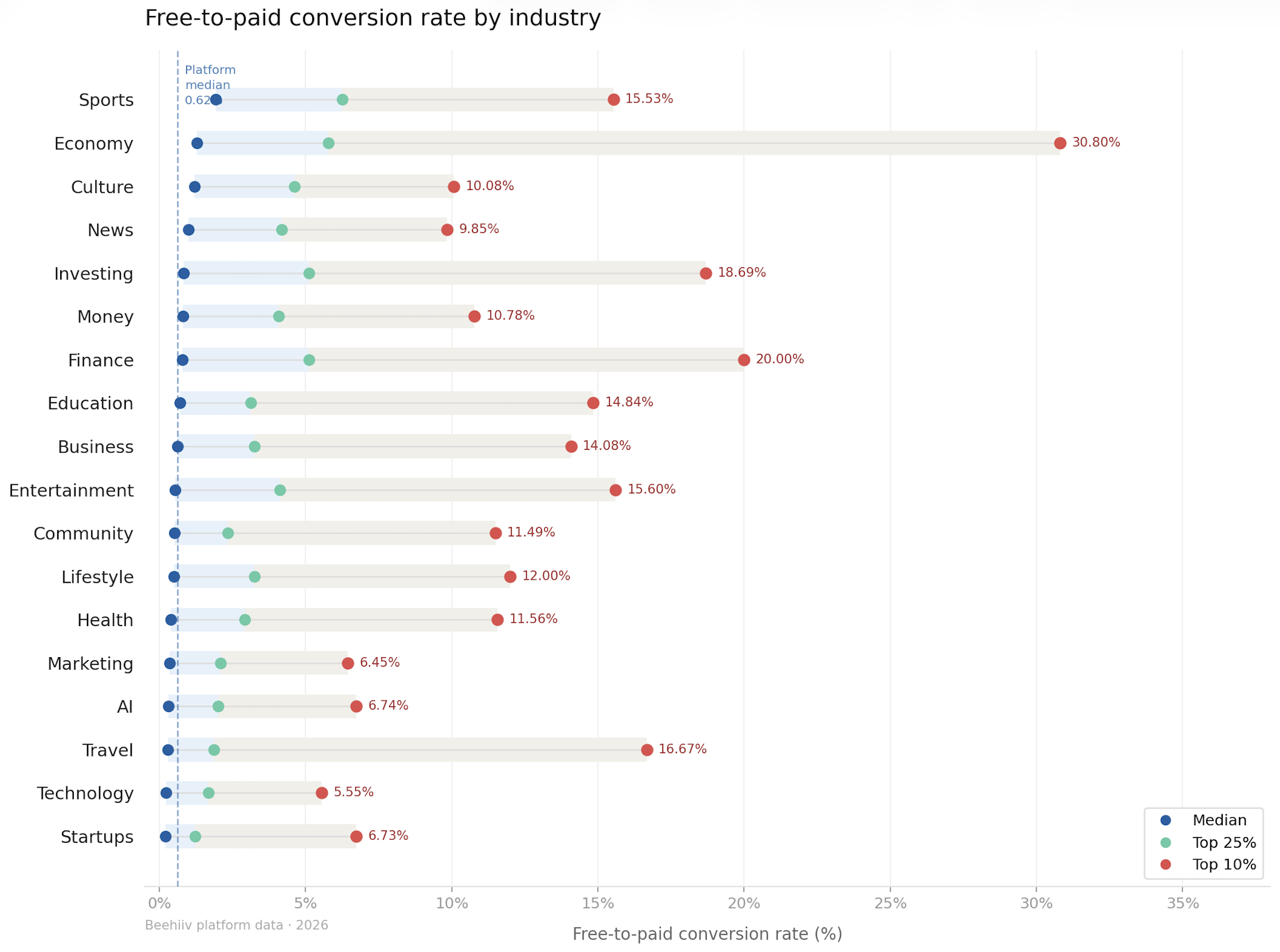

One of the most surprising data points from Beehiiv’s report pertained to A.I. newsletters—not newsletters

written by A.I., but newsletters about A.I. On Beehiiv, the category is the fourth-largest paid segment, with 301 publications, just behind general technology (305), finance (400), and business (634). Despite their popularity, A.I. newsletters also have some of the lowest free-to-paid conversion rates, with a median of about 0.3, putting the topic in the bottom five of all major industry newsletters. By comparison, the conversion rate for the top 10 percent of A.I. newsletters

sits at over 6 percent. |

A.I. is arguably the perfect illustration of a broader trend: An uptick in general interest around a

given topic doesn’t necessarily lead to a commensurate uptick in paid subscribers. Not only are the conversion rates for A.I. newsletters on Beehiiv much lower, but their churn rate is 13.3 percent, making A.I. one of the leakiest categories on the platform. It’s not necessarily because the content isn’t good, but rather because there’s so much of it, including on free tech websites and within all-access news subscriptions.

When there are so many newsletters offering the same or similar

content, individual products need to either hyperfocus on a specific aspect of a hot topic (Lenny Rachitsky’s concentration on A.I. and productivity or Azeem Azhar’s Exponential View, which includes consultant-level data analysis) or have built-in fan bases. Case in point: Kevin Roose and Casey Newton, who are leaving the Times and ending their Hard Fork podcast to launch their own media venture.

|

3. Content Is King, Community Is Kingmaker

|

“Community” has quickly become one of those ubiquitous and appalling buzzwords tattooed on the neck

of the modern media industry. Morning Brew’s Austin Rief has claimed that community will do more for media revenue and brand development in the next 10 years than content creation did in the previous decade. New New York magazine owner James Murdoch has been acquiring community through acquisitions of the Tribeca Film Festival and Art Basel. Atlantic C.E.O. Nick Thompson is taking readers on cruises. And John

Fulton’s Eastside Rag, a newsletter with more than 6,000 subscribers, is accidentally playing matchmaker. Seriously.

The data from Beehiiv explains why the topic continues to vex media executives. While subscriptions are still the top revenue driver for Beehiiv’s paid creators, community memberships make up a growing part of the pie, per the report. This can include access to exclusive Discord groups, early access to events, or meetups, which Emily Sundberg has

perfected. The Free Press has gotten into this game, too.

The value of community can’t be artificially manufactured. If audiences don’t feel a personal connection to the author or share intimate experiences with other members in the group—all of whom understand the same callback joke, or remember the same personal story—then they’ll drift elsewhere. And yet one of the challenges of this dynamic is that it’s hard to produce at scale. The journeys of Substack and Beehiiv suggest that most

creators never make it to the level where they’ve built an authentic community. And those who have must hire operators and employees to pour as much attention into events as they have into their own writing. For all the attention paid to the newsletter economy, there are still few experts who know what it really leads to. |

|

|

|

A professional-grade rundown on the business of sports from John Ourand, the industry’s preeminent journalist, covering the

leagues, players, agencies, media deals, and the egos fueling it all. Plus, the latest intel from Eriq Gardner on the sports legal beat. |

|

|

|

Join Puck’s chief political columnist, John Heilemann, as he roams the corridors of power and influence in America on this

twice-weekly interview show, taking you beyond the headlines with the people who shape our culture: icons and up-and-comers, incumbents and insurgents, moguls and machers in the overlapping worlds of politics, entertainment, tech, business, sports, media, and beyond. The conversations are rich and revealing, unrehearsed and unexpected… and reliably impolitic. A Puck-Audacy joint, new episodes drop every Wednesday and Friday. |

|

|

|

Need help? Review our

FAQ page or contact us for assistance. For brand partnerships, email ads@puck.news.

You received this email because you signed up to receive emails from Puck, or as part of your Puck account associated with {{customer.email}}. To stop receiving this newsletter and/or manage all your email preferences, click here. |

Puck is published by Heat Media LLC. 107 Greenwich St., New York, NY 10006 |

|

|

|

|