|

|

Welcome back to Dry Powder. I’m Bill Cohan.

|

|

Thanks, as always, for reading. Before jumping into today’s issue, I want to shout out my brilliant Puck partner Tara Palmeri for inviting me onto her stellar podcast, Somebody’s Gotta Win, to talk about Trump’s lucky break at the N.Y. appeals court and the post-SPAC fate of Truth Social. You can listen to that episode here.

Tonight, a timely eulogy for the end of the Jack Welch era in American business as Dave Calhoun, one of Jack’s acolytes at GE, is pushed out as C.E.O. of Boeing after a dismal four years.

But first….

- The Great Proxy Fight of 2024 is coming to a head!: Nelson Peltz, the octogenarian co-founder of Trian Management who controls 32.27 million Disney shares, enjoyed a couple recent pyrrhic victories in advance of his April 3 proxy fight. Last week, Institutional Investor Services, a big proxy advisory firm, recommended that Disney shareholders vote for Trian’s slate of two directors, including Peltz and the former Disney C.F.O. Jay Rasulo. And this morning, Egan-Jones, a smaller proxy advisory firm, also recommended that shareholders support Nelson and Rasulo.

But that’s about it. Bob Iger, the Disney C.E.O. in his second tour of duty at the company, is winning more support than Peltz. Another big proxy firm, Glass Lewis, is in Iger’s corner, as well as members of the Disney family, including Abigail Disney, who has been highly critical of the company, and large Disney shareholders George Lucas and Laurene Powell Jobs. Iger is also benefiting from the fact that the Disney stock is up more than 31 percent so far in 2024. That’s good news for both Iger and for Trian, since the hedge fund is now well into the money on its Disney shares.

Of course, it’s not so good for Peltz’s argument that he should have two seats on the Disney board in order to shake things up. As I have written previously, Peltz’s lengthy “white paper” on Disney, released a few weeks back, was very good at diagnosing Disney’s myriad of problems, but wishy-washy when it came to suggesting meaningful and actionable solutions. And he never got to the crux of the matter, which was why the Disney board of directors, with Iger’s support, chose Bob Chapek to succeed Iger (briefly) as the pandemic was getting going. That was a serious miscarriage of judgment on the part of the Disney board, but Peltz has never focused on that major error.

Peltz probably thought his recent barrage of interviews in the mainstream media—among them, profiles in the Times, the Journal, and the FT—would do him some good in his proxy campaign. But he came off as arrogant and exceedingly tone deaf. For instance, the Times let him get away with saying he has never been responsible for firing any C.E.O.s of the companies in which Trian has invested. However, Trian was directly responsible for firing Jeff Immelt at GE and replacing him with John Flannery, and was responsible for defenestrating Flannery and replacing him with Larry Culp. Peltz was also the invisible hand behind the elimination of Ellen Kullman, as the C.E.O. of DuPont.

Peltz’s “Lunch with the FT” was also disastrous. He asked Harriet Agnew, the writer of the piece, why Disney made The Marvels and Black Panther movies the way that it did. “Why do I have to have a Marvel that’s all women?” he said. “Not that I have anything against women, but why do I have to do that? Why can’t I have Marvels that are both? Why do I need an all-Black cast?” He’s also said he dislikes Donald Trump, abstained from voting in 2016, but then held a fundraiser for Trump in 2020 and then turned on him again after January 6. Now he’s all in on Trump again—although, he told Agnew, “I’m not happy about that.”

All told, the proxy fight will cost both sides around $75 million by the time April 3 rolls around. As I have written recently, I don’t get these proxy fights anymore. They are a huge waste of money and even if Peltz were to win—and he won’t—he’d only get two seats on a 12-member board. Thankfully, it’ll all be over in another week or so.

- Trump’s lucky streak: What won’t be over in another week or so, alas, is the inane saga of the Luckiest Man on Earth, Donald Trump, and the idiotic combination of Truth Social, Trump’s personal version of Twitter, and a ridiculous shell company, a SPAC known as Digital World Acquisition Corp. After some two years of futzing around, the DWAC shareholders have approved the merger with Truth Social and it started trading as a public company, with the ticker DJT, on Tuesday. This came at the very same moment that Trump looked like he wouldn’t be able to gin up the cash to pay the $500-million-plus bond that he needed to appeal his civil fraud case in New York State. But he got lucky twice on Monday. The merger between Truth Social and the SPAC became official, and a New York State appeals court lowered his bond amount to $175 million and gave him another 10 days to come up with the money. Presumably, he’ll be able to do that in short order.

The meme stock started trading on Tuesday and immediately shot up some 45 percent! This is not investment advice, but in nine months of 2023, Trump Media & Technology Group, the parent company of Truth Social, generated revenue of a meager $3.4 million (not a typo) and lost $49 million. DWAC, of course, was an empty shell company with nothing in it but the cash it raised from its I.P.O. And yet DJT was worth around $13 billion (also not a typo) during the day on Tuesday before settling down to be valued at around $8 billion. (It was back up to $9.5 billion today.) And, equally incredibly, Trump’s 79 million shares in DJT were worth a whopping $5.8 billion, before settling down to around $4.5 billion. (And now worth $5.3 billion.) Only Donald Trump could turn his mindless bloviating into $5 billion.

On the other hand, Trump can’t sell his stake in DJT and turn it into cash for at least another six months, unless the board of DJT decides to give him a waiver. And it might, considering the board, as of Monday, consists of his son, Donald Jr., as well as Trump acolytes Robert Lighthizer, his former trade representative; Kash Patel, who nearly got big jobs at the C.I.A. and F.B.I. under Trump; and Linda McMahon, the head of the Small Business Administration under Trump and the wife of the founder of World Wrestling Entertainment. Devin Nunes, the former congressman and Trump defender, is also on the board. He was C.E.O. of Truth Social after he left Congress.

This surely is a board that will allow Trump to do what he wants. But even Trump is smart enough to know that when he starts selling his shares, the bloom will be off the rose and the stock will trade down, probably precipitously. Of course, he may not care about that, as long as he is able to get some money out of this joke of a SPAC. He certainly cares less about owning DJT than he does about owning Trump Tower or 40 Wall Street or Mar-a-Lago or Doral. So if he ends up losing his appeal of the New York State verdict, and has to pay the $500 million-plus to the state, you can bet your bottom dollar he will make that payment using the DJT stock long before he lets Letitia James, the New York State Attorney General, get her hands on his other “trophy” assets.

|

|

| The End of the Jack Era |

| Dave Calhoun’s forced exit from Boeing is the final vestige of Jack Welch’s nearly 50-year influence over Wall Street and American corporate life. |

|

|

|

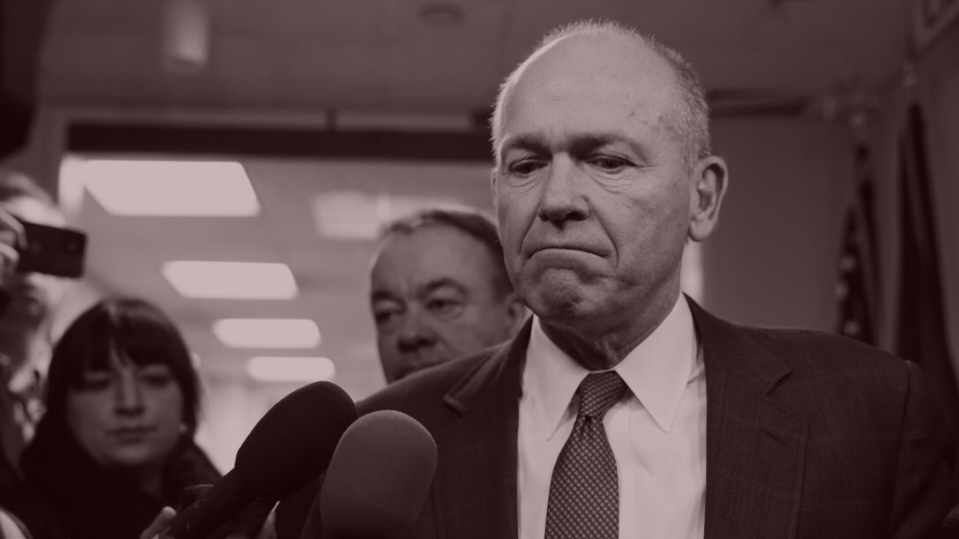

| The defenestration of Dave Calhoun, who will step down as the C.E.O. of Boeing by the end of 2024 after only four short years, gives our national champion aircraft manufacturer the chance it needs to reset following one mishap after another. Calhoun, of course, was hoping to fix the mistakes made by his predecessors—in particular, the embarrassing and deadly mishaps related to the 737 Max jet—but he was not able to do it sufficiently before another series of flubs occurred, exacerbating his hasty departure. His critics have not been kind. “Just what did Calhoun think he was accomplishing during his four year tenure as Boeing’s C.E.O. fixer?” Mark Cohen, a professor at Columbia Business School, my alma mater, asked me rhetorically on Monday. “He accomplished nothing.”

It’s hard to argue with Cohen. Boeing’s stock has fallen roughly 50 percent during Calhoun’s tenure at the company. Something had to change. And Calhoun’s exit, along with the chairman of the board of directors and the head of the commercial airplane division, turned out to be the change that was needed.

But Calhoun’s end at Boeing also signifies something even more profound than just the departure of another C.E.O.: It marks the end of the Jack Welch era in American business, one that has spanned more than 40 years, starting from when Welch became the C.E.O. of General Electric in 1981 and held the position for the next 20 years, until September 2001. Under his tenure it was the multi-headed leader in finance (GE Capital), media (NBCU), industrials and more—and, of course, the most valuable company in the world.

Under Jack, GE also became legendary as a breeding ground for superior corporate managers, who were much sought after by companies all around the world. The two men who lost out to Jeff Immelt in the race to succeed Jack both became C.E.O.s themselves: Jim McNerney at Boeing (several C.E.O.s before Calhoun and after his stint as C.E.O. of 3M); and Robert Nardelli, first at Home Depot, then at Chrysler. The list of corporate C.E.O.s who once worked at GE is long, and impressive.

But the GE halo seems to be ending along with GE, itself: Calhoun’s departure coincides with the final nail in the coffin for GE, which was founded by a big merger between two cutting-edge electric generation businesses in 1892, and was our leading industrial company for most of the 20th century. Soon enough, GE will complete its split into three companies: the healthcare business is already trading publicly, and the power business is about to start trading on April 2, leaving only the jet engine business as what was once known as GE. (Immelt had years earlier sold off both GE Capital and NBCU.)

In many ways, Calhoun epitomized the ultimate GE man. He was one of Jack’s guys. After graduating from Virginia Tech in 1979, with a degree in accounting, he had a choice between working for GE in Philadelphia and working for Westinghouse in Pittsburgh. Back then, as he told me for an interview for my 2022 book, Power Failure, the two companies “were identical, identical.” Since he had grown up in Allentown, he decided to take the GE job to be closer to home. He joined the elite Financial Management Program, which trained recent college graduates over two years in the fundamentals and the nuances of finance, and put their GE careers on a higher trajectory. After Calhoun excelled in the FMP program, Dennis Dammerman, the GE C.F.O., asked him to go to GE Capital, in Stamford, to work for the group that was financing leveraged buyouts. He then worked as a staff executive to Larry Bossidy, Jack’s right-hand man until Bossidy decamped to become C.E.O. of Allied Signal. “That was a training job,” he said. “That was me working with the C.E.O.s of all of the businesses Larry looked over and trying to help them do projects and trying to keep a finger on GE Capital.”

Then Jack started taking control of Calhoun’s career: After Calhoun worked for Bossidy, Jack put him into the same job at the Plastics division, in marketing, that Immelt had once had. “That was a coveted job,” Calhoun said. He found himself in that group of executives whom Jack moved from job to job to test their mettle. Calhoun asked Jack to consider sending him to Asia when it came time for his next move. Jack obliged. “I could see that that was exciting and the future, and there was a resourcefulness required that I don’t think GE folks were practiced at,” Calhoun said. “I figured I’d better put myself in that situation if I could.”

|

|

|

| From there, Calhoun had big jobs in GE’s locomotives division, and then as the number two to McNerney at jet engines when McNerney was under serious consideration to succeed Jack. Calhoun, GE’s best golfer, played often with Jack, who was also an excellent golfer, and the two often spoke about the GE succession competition while on the golf course. “The selection of Jeff at that time was not a bad call,” Calhoun told me. “If you’d have pinned me in a corner and said which of the three, I probably would have said Jeff.”

When Jeff Immelt got the job and McNerney left for 3M, Calhoun became head of the jet engine division, the job he had when Jeff took over right before September 11. On the morning of September 11, he and Immelt had a meeting scheduled in Seattle with Phil Condit, the C.E.O. of Boeing, that was quickly canceled after the attack. GE had not only made the engines on the Boeing jets that crashed into the towers, it also owned NBC, which broadcast the horrors, and had reinsured, through GE Capital, at least one of the buildings at Ground Zero.

For a while after Jeff became C.E.O., Calhoun’s name was one of three in the envelope that the board kept handy in case Jeff got hit by a bus. The other two names were John Rice, who had been head of both GE’s power business and its transportation business, and C.F.O. Keith Sherin. Jeff had to reflect on the names on the envelope every year—in case he died or got “whacked,” as he said—and so they would change every now and then.

In June 2005, as part of another corporate reorganization that reduced GE’s businesses from 11 to six, Jeff named Calhoun a GE vice-chairman and head of GE Infrastructure, which included aviation, power, transportation, oil and gas, wind, and water—a big job, perhaps the biggest at GE, aside from Jeff’s. “I bent myself into a pretzel to keep Dave,” Jeff told me for the book. “And he knows it.”

At the time, Calhoun was one of the most sought-after potential C.E.O.s in the country: “The No. 1 draft pick in the game of grabbing top executive talent,” was how Fortune once described him. It was Calhoun’s enviable combination of intense competitiveness, global business experience, and knowledge that he would never succeed Jeff as GE C.E.O.—they were too close in age—that made him a headhunter’s dream. He also feared being part of GE’s lavish supplemental pension program, which paid top GE executives big bucks—Immelt, for one, still gets $5 million a year from that program—but often turned them into milquetoasts, fearful that one wrong word to the C.E.O. would jeopardize that benefit. Calhoun decided to leave GE before he became eligible for that windfall. That was courageous.

Calhoun said he saw “early signs” of trouble at GE under Jeff’s stewardship. “I’ve stayed close enough to everybody to sort of watch it unravel,” he said. It didn’t happen overnight. “It took all of fifteen years to do it,” he said, adding that if anyone had raised his or her hand during the first eight years, “a lot of it was fixable.” But no one did, in part because Jeff didn’t like to hear dissent or bad news and praised loyalty, perhaps to a fault. Or maybe it was out of fear of losing the supplemental pension benefit. Plus, as ever, it was very difficult to push back on a C.E.O.—unless that C.E.O., like Jack, mostly encouraged and rewarded outspoken executives. With Jeff, “it was impossible,” Calhoun said.

In August 2006, Calhoun left GE to become the chairman and C.E.O. of VNU, a media company that controlled A.C. Nielsen and Billboard magazine, among others. VNU had been purchased earlier in the year by a consortium of private equity firms, including Blackstone, KKR, Hellman & Friedman, and the Carlyle Group. Calhoun’s pay package was estimated to be around $100 million. After successfully turning around VNU and leading its I.P.O. in 2010 as Nielsen Holdings, Calhoun left the company in 2013 and became an operating partner at Blackstone, which was where he was when I interviewed him. In 2020, he became chairman and C.E.O. of Boeing, after serving on the company’s board for many years.

Calhoun’s departure from Boeing marks the end of the Welch chapter in American corporate life. Immelt is long gone from GE. McNerney is also gone from Boeing. Nardelli is gone from Home Depot and Chrysler. Dave Cote is long gone from Honeywell. Gary Wendt is long gone from GE Capital. Larry Bossidy is long gone from Allied-Signal, what is now Honeywell, which Jack almost bought in 2001 before he left GE. And, of course, Jack died in March 2020, right before the worldwide pandemic started. His funeral at St. Patrick’s Cathedral, on Fifth Avenue, was one of the last public events before Covid changed everything. Needless to say, it was quite a collection of the rich and powerful—the final curtain on an era in American business that had been fading for years, and now has ended at last.

|

|

|

|

| FOUR STORIES WE’RE TALKING ABOUT |

|

| Shanahan’s Ascent |

| The definitive bildungsroman of R.F.K. Jr.’s V.P. pick. |

| TEDDY SCHLEIFER |

|

|

| Putin’s New Trick |

| How the Russian propaganda machine is spinning the Moscow terror attack. |

| JULIA IOFFE |

|

|

|

|

|

|

|

|

|

|

|

|

|

Need help? Review our FAQs

page or contact

us for assistance. For brand partnerships, email ads@puck.news.

|

|

You received this email because you signed up to receive emails from Puck, or as part of your Puck account associated with . To stop receiving this newsletter and/or manage all your email preferences, click here.

|

|

Puck is published by Heat Media LLC. 227 W 17th St New York, NY 10011.

|

|

|

|