Hello and Happy Disney+ Day Eve.

We’ve got a Disney-centric What I’m Hearing today, and thanks to the Inner Circle members who joined Dylan Byers and myself for our chat about Mark Zuckerberg and the Metaverse this afternoon. We’ll be doing more of these, so if you’ve got topic suggestions, let me know at matt@puck.news.

Reminder: If this email was forwarded to you, sign up for Puck here. (Yes, we have group subscriptions, just email fritz@puck.news.) Thanks again for your support.

Before we begin…

Sponsored by Amazon Prime Video

Thursday Thoughts…

Also, today I’m welcoming Julia Alexander, a new occasional contributor to Puck and the What I’m Hearing private email. Julia is a super smart strategy analyst at Parrot Analytics, which measures digital content consumption, and she’s a journalist who has done great work at outlets like The Verge and IGN. Because Julia is an expert on all things streaming and Disney, for her first piece I asked her to look at what the data says Disney+ needs to do next. Scroll down for that.

But first, here’s my take on the new reality for Disney after the brutal numbers revealed yesterday…

Disney’s disappointing fourth quarter underscores the risk, and the unforgiving new reality, for entertainment companies that have hitched their share price to ceaseless subscriber growth. Well, now we know why Disney scheduled a big promotional stunt two days after its fourth quarter earnings reveal: C.E.O. Bob Chapek knew the Disney+ subscriber numbers would stink like Donald Duck’s diaper—he telegraphed as much in September—and with all those annual subscriptions up for renewal, tomorrow’s “Disney+ Day” was born. I trust you’ll be dressed appropriately and celebrating your toddler’s favorite Moana delivery app with the fanfare Chapek expects, paying no attention to the Disney stock slide of 7.4 percent since yesterday, down 20 percent from a March peak. Its market cap is now at $294.6 billion, about the same as Netflix.

For better and worse, that’s the new reality for Disney’s shares, which thrived during a pandemic that crippled its parks and movie businesses because investors were convinced that it was becoming a tech company. Disney stock is still trading at a crazy-high multiple, all because that’s how Netflix trades, thanks to strong growth in subscribers. Problem is, that narrative requires that Disney+ actually keeps growing at a healthy clip, which, with just 2.1 million new subs this quarter, well below some analyst estimates of 9 million, it most definitely is not. Never mind that the company’s other divisions all rebounded well from the pandemic comps of a year ago. Even the most Disney-drunk analysts cut their price targets, and a Marketwatch headline declared yesterday “the most disappointing earnings report in 10 years.” Live by the sub, die by the sub.

Disney isn’t alone in this predicament, of course. Streaming is the digital horse to which every entertainment company has hitched its wagon, and it’s far from clear whether the wagon train will eventually roll off a cliff. That said, it’s an especially strange era for Disney, which has always been the envy of Hollywood because it is not solely dependent on one business, or even a small number of businesses. Walt’s famous flywheel enables not just synergies among interlocking units but cushions when, say, the movie division releases a few expensive turds, or a recession kneecaps parks and cruises.

But no more: It’s streaming or bust, ignore all the other stuff, flywheel be damned. And that’s creating some potentially dangerous incentives for Chapek. As the other Bob, he’s never going to win a statesman of the year contest, nor is he known as an M&A specialist, or a creative visionary (or even particularly friendly with creatively-talented people, say those who know him). He’s a manager, first in home video, then at the studio, then in consumer products, then parks, and finally as lead Mouseketeer. The stock price is his primary job, as it is for all C.E.O.s, but especially for those without that other stuff. If subs don’t rebound and the stock continues this slide, he’s going to start throwing everything but the Seven Dwarfs’ kitchen sink at Disney+.

ADVERTISEMENT

Prime Video presents the Amazon Original Limited Series THE UNDERGROUND RAILROAD, from Academy Award winner® Barry Jenkins and starring Thuso Mdebu and Joel Edgerton. Winner of 2 AAFCA awards for Best Limited Series and Best Director Barry Jenkins, and now nominated for 2 Gotham Awards for Best Breakthrough Series — Long Form and Outstanding Performance in a New Series, Thuso Mbedu. Good Morning America raves the series is “a flat-out masterpiece, Jenkins has raised series television to the level of art.”

THE UNDERGROUND RAILROAD is awards eligible and available at ConsiderAmazon.com.

Yes, I know, Chapek already is heavily prioritizing D+ at the expense of everything else. But the shift could become even more dramatic very soon. For instance, Chapek hasn’t committed to an exclusive theatrical window for Disney films beyond the end of next month. Marvel’s three likely blockbusters set for next year—sequels to Doctor Strange, Thor, and Black Panther—must look mighty attractive for “premiere access” day-and-date releases, or even direct-to-D+. Pixar’s Turning Red seems all but a shoo-in for D+ only, given Soul and Luca were released that way. But what about Lightyear, the big Toy Story prequel with Chris Evans? People at Pixar are hopeful that one will get a theatrical window, given its box office prospects. Is Chapek? To investors yesterday, he preached only “flexibility.”

That may be the right strategy for short-term sub gains, and analysts would likely cheer, but it would come at the expense of potentially billions of dollars in box office revenue and the long-term franchise-building associated with theatrical releases. (Not to mention all the talent and executive headaches that came with 2020’s day-and-date experiments.) Still, since Netflix became the darling of entertainment stocks, the market has shown that it will reward only one measure of success. It would be silly to think Chapek won’t follow the market as aggressively as possible.

So, what should Disney actually do to increase Disney+ subscribers? Julia Alexander has some thoughts based on industry consumption data, including her own work at Parrot Analytics, which tracks various consumer actions to measure popularity of content by “demand” expressions…

How to Fix Disney’s Sluggish Streamer: It’s All About the Hamiltons By Julia Alexander

OK, but what else have you got?

It might be strange to say that about Disney+, which sits at 118 million subscribers after exactly two years of existence. Its family programming amounted to nearly 17 percent of total “demand share” for kids content in the U.S. during October, according to Parrot Analytics data, second only to Nickelodeon. At the same time, each live-action Marvel and Star Wars series on Disney+ has become the most in-demand show globally within weeks—and in some cases days—of premiering, far outpacing competitors.

Except that is the question these days. During the company’s earnings call yesterday, Disney C.E.O Bob Chapek revealed a notable Disney+ subscriber slowdown, adding just under 2 million customers in the quarter. The stock tanked, and questions are growing about the scalability of the service, as well as the nearly 40 percent of subs coming from Disney+ HotStar in India, where revenue per subscriber is lower, and where usage is driven by regional sports that could be scooped up by a rival.

Disney observers increasingly want to know: How can Disney+ continue growing beyond the families who subscribe for kids (and who likely signed up immediately), and the Star Wars or Marvel diehards (who likely were already lured)? Or, as I like to refer to it, how does Disney+ recreate its Hamilton magic?

Some quick context. In July 2020, when Disney+ premiered the filmed version of Broadway’s Hamilton, millions of new customers signed up. Specifically, there was a 641 percent increase in Disney+ subs that weekend compared to prior weekends, according to analytics firm Antenna. More important to Disney, however, was who signed up. Unlike the first rush of 10 million customers on Disney+ launch day, those new subs weren’t convinced they needed to watch a new Star Wars show or library titles like Moana or Up. Hamilton, however, was new, exclusive, all-audience, and generated just enough anticipation to convince unsure customers to finally give Disney their credit card info.

But as significant as that rush was the subsequent drop-off. Roughly 30 percent of customers who signed up for Disney+ during Hamilton’s premiere weekend (July 3, 2020) canceled their subscription after one month—or, to put it another way, they were 1.5 times as likely to cancel than other customers, according to Antenna.

There just wasn’t much else for them. They came in for what they wanted—Lin-Manuel Miranda’s blockbuster musical to watch while stuck at home over Independence Day in the middle of a pandemic—and many bolted as soon as possible. It’s a somewhat similar predicament for many who come for WandaVision or The Mandalorian. What else is there to watch that isn’t more of the same?

ADVERTISEMENT

At the heart of Disney+ is the Disney brand, and that’s never going to change. But to reach 230 to 260 million global subscribers by the end of 2024, which Chapek and C.F.O. Christine McCarthy projected last December and re-committed to on Wednesday, the service must appeal to the Disney crowd and then some.

Chapek seems to know this. “Disney+ is a four-quadrant service, and as such, we need content that is going to be broad and appeal to each of those demographics,” he told investors yesterday. “That’s why we’ve fired up the production engines of our Fox team … Searchlight … and our general Disney Channel entertainment team, making content both for Hulu and Disney+.”

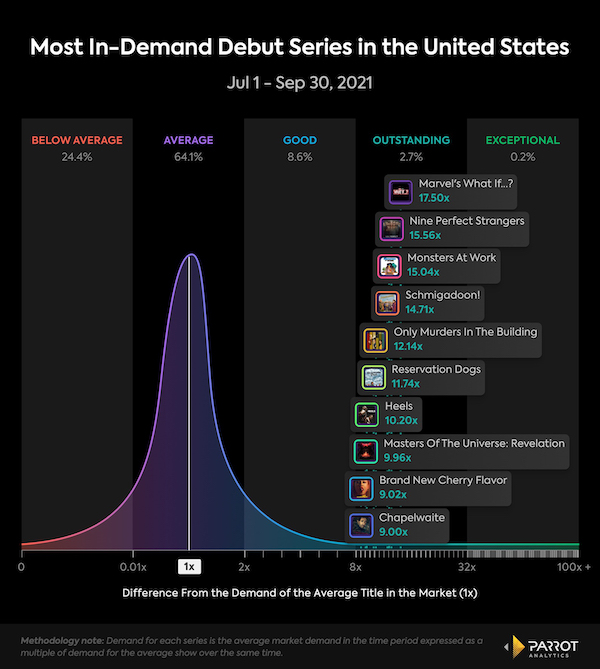

Demand for Hulu and Disney+ Originals over the last quarter. You'll notice that there are three Hulu originals, and two in particular that are very different from Disney+ offerings. These titles are likely to bring in new customers because they're different from Disney+'s core offerings (currently). That sounds good, but the fact is, Disney+ is not currently a four-quadrant service, meaning it is not a must-have for all audiences, young, old, men and women. Not on its own, at least. For instance, recent studies from HarrisX, per a MoffettNathanson note, demonstrate that Disney+ suffers from poor adoption rates by older viewers. The lack of a diverse slate, in addition to a relatively bare cupboard (just over 1,300 titles, compared to close to 8,000 at Amazon Prime Video) means that Disney+ engagement time per session for non-children is likely much lower.

The company’s solution for this in some territories (Europe, Canada, Australia, New Zealand, and Singapore) is Star, the Disney+ add-on with content from FX, ABC, Freeform, and other Disney networks that fuel Hulu in the U.S. When shows like Modern Family or Dopesick are available directly within an app, it takes less effort, commitment, and dollars to keep customers streaming. Everything is in one place. If users in the U.S. want to jump from Loki to Only Murders in the Building, they must make an affirmative effort to leave Disney+, search for the content, then open Hulu (including signing up for it individually or through a bundle), before watching it.

Disney+ with Star creates one general entertainment offering—everything for someone, while also carrying something for everyone. Chapek and Co. want the so-called “Disney bundle” (D+, Hulu without ads, and ESPN+ for $20) to solve this issue. It might, but the value proposition for the bundle is still three streaming services for the price of two, instead of two streaming services for the price of one.

Having an entire library of content spread out across two different streaming services also interferes with context-driven feedback recommendations, a key component to increasing session time and making a platform like Disney+ feel like a necessity, even when the Frozen 2 or Hawkeye credits roll.

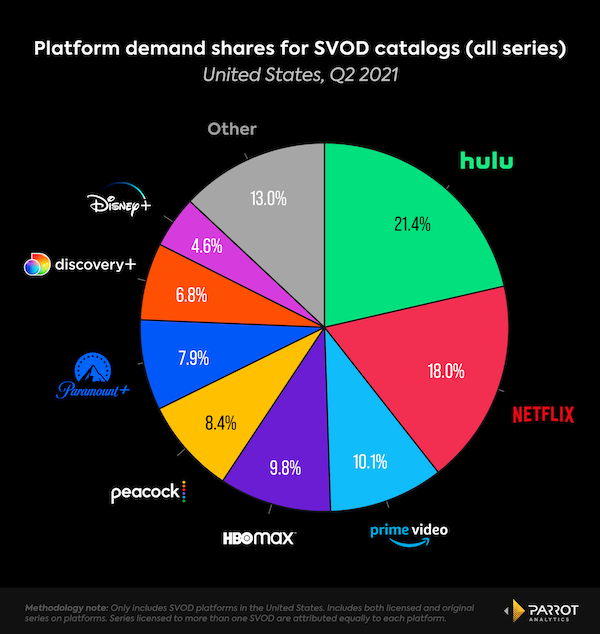

Hulu actually has the most platform demand shares for SVOD catalogs - which is a fancy way of saying that the demand across the entire catalog is higher than any other. Netflix is in second, but you'll notice that demand for Disney+'s catalog is actually at the bottom of the ones listed. While not all of Hulu's catalog is exclusive to Disney+ (a lot of Comcast), it's still pretty significant. Subscribers who might want to watch Nine Perfect Strangers after, say, Hamilton, aren’t seeing that title because it’s on an entirely different app, despite being part of the same bundle. If Nine Perfect Strangers was on Disney+ and recommended to Hamilton fans while they are wiping away tears at the end of “Who Lives, Who Dies, Who Tells Your Story,” they would likely stay on the platform longer—and would be less likely to churn out. Making a wider array of general-entertainment content available, and ensuring the right customer sees the right recommendation, would cement Disney+ as a necessity to a lot more people.

“Perceived value” is essentially how much a customer thinks something is worth. It’s why someone decides that HBO Max is worth $15 a month—because it’s the price of HBO with a bunch of extras thrown in. By contrast, “real value” is how necessary a service is to a subscriber, looking at all the individual parts associated with the monthly cost.

Apply these standards to Disney+. If the perceived value of Disney+ is that it provides daily entertainment for $8 a month, with a slew of new originals and lovable favorites, but customers find themselves only opening it once every two weeks, then the real value is far less than its original perceived value.

Disney’s “high acquisition” originals (meaning, it has a lot of breakout series that bring in swaths of new subscribers, like The Mandalorian) come from the company’s franchise pillars. Multiple new Star Wars, Marvel, and Pixar projects hit the service throughout the year. But these series all have extremely high affinity with one another—those who watch The Falcon and the Winter Soldier are probably watching some combination of WandaVision, The Mandalorian, Loki, Star Wars: Visions, What If…?, and The Mighty Ducks.

The Disney+ churn rate is below industry standard (4.3 percent, compared to 6.8 percent for HBO Max, and 9.5 percent at Peacock, but more than Netflix’s 2.5 percent, as reported by Variety). So debuting a new Marvel or Star Wars series every few weeks is great for retention purposes. It’s not great for continued growth among the millions of people who don’t want to watch every new Star Wars or Marvel title. It’s also not great for customers without children who are looking for general entertainment. How does Disney get the Hamilton crowd back?

The answer is that Disney+, in territories where Star isn’t offered, needs new Hamiltons, or even Dopesicks, on the platform with greater frequency—not on a different platform that exists within a bundle. It’s a double edged sword for Disney; having racier content on a service that kids may accidentally access is counterintuitive to Disney branding, and offering a “Star” tab would siphon subscribers from Hulu—and Disney’s effort to upsell a bundle that includes a service Disney executives have made clear is a core part of the company’s streaming empire. (Disney is set to complete its full acquisition of Hulu in 2024, paying Comcast billions of dollars for the company's remaining 10 percent stake.)

Without it, however, Disney+ misses out on key programming opportunities that its competitors are pumping billions of dollars into producing. Adding more general entertainment would greatly expand what subscribers and potential customers think Disney+ is offering, and widen the customer base that Disney+ can attract.

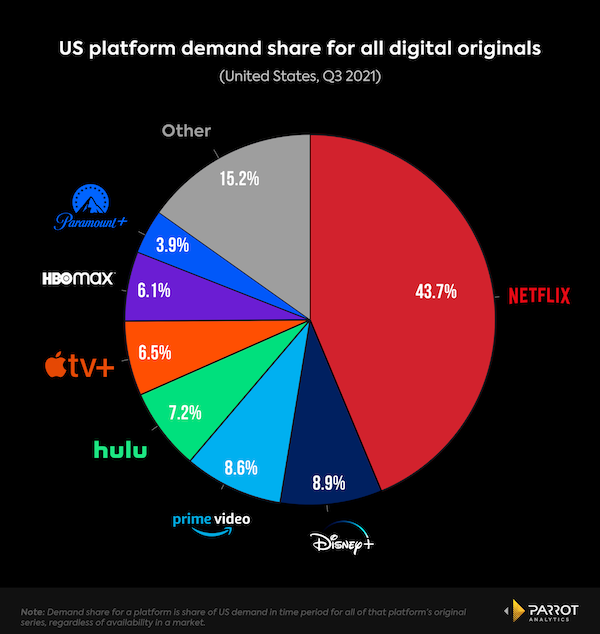

This is the platform demand share for all digital originals in the US over the last quarter. Notably: Disney+ has jumped into second place over Amazon Prime Video, and Hulu is in fourth place. Hypothetically, if Hulu and Disney+ existed as one platform, the platform demand share would be lightyears ahead of most competition save for Netflix. The counterargument, of course, is that Disney+ has reached 118 million subscribers thanks to families and just a few core franchises. Even if growth slowed this quarter to less than 2 percent in total subscribers, those numbers are still increasing. For as long as there are children and superfans, Disney+ will have a sizable subscriber base.

This is true, but it’s not the full picture. Disney+ has the advantage of a century of content and IP. But Disney isn’t the only company trying to use franchises to grow to 250 million global subscribers. Netflix is investing billions of dollars on kids content, for instance, including targeting six animated feature films a year—more than Disney releases between both its Disney Animation and Pixar units. Apple is working with Skydance Animation on projects for children, and that’s on top of acquiring the Fraggle Rock library and producing more Peanuts specials. WarnerMedia has Cartoon Network, Looney Tunes, and Sesame Street, all of which are seeing increased investment.

Disney may be king, but competition is fierce. Where Disney+ succeeds, competitors are trying to catch up—and where Disney+ lags, competitors are lightyears ahead. For the service to grow beyond kids, fanboys, and Indian cricket lovers, it must become more of a general entertainment platform. It needs a little bit of Marvel, a little bit of Pixar, and a little bit of Only Murders in the Building.

See you Sunday, Matt

Got a question, comment, complaint, or a fun lunch sighting? Email me at Matt@puck.news or call/text me at 310-804-3198.

FOUR STORIES WE'RE TALKING ABOUT With the Chappelle uproar, Netflix has become an unwitting signpost in the culture wars. Some believe it may presage a turning point. MATT BELLONI Yes, Critical Race Theory helped Glenn Youngkin defeat The Macker. But the behind-the-ballot-curtain reality is more complex. PETER HAMBY As global supply chains break down, the U.S. Department of Energy faces a political-economic crisis of its own making. PETER HAMBY Tesla has broken the will of short-sellers, market prognosticators, even the all-seeing Michael Burry. But is the party finally ending? WILLIAM D. COHAN

You received this message because you signed up to receive emails from Puck.

Was this email forwarded to you?

Sent to {{customer.email}}

Puck is published by Heat Media LLC.

For support, just reply to this e-mail. For brand partnerships, email ads@puck.news |

SHARE