|

|

Welcome back to What I’m Hearing+, live from Brooklyn, where I’ve been reunited with the constant sound of sirens after a peaceful weekend upstate. I’m headed to Florida for some client events, Disney World, etcetera, so please send your best recommendations. My only real mission is building a lightsaber.

The coming “Spulu” sports bundle has forced many, including my clients, to ponder the uncertain fates of the Max sports add-on and Disney’s ESPN+. Tonight, I’m contemplating an even larger question: Amid all the chaos, which streamers might not be here next year? Should Amazon sunset Freevee? Why does Discovery+ still exist? And much, much more.

But first…

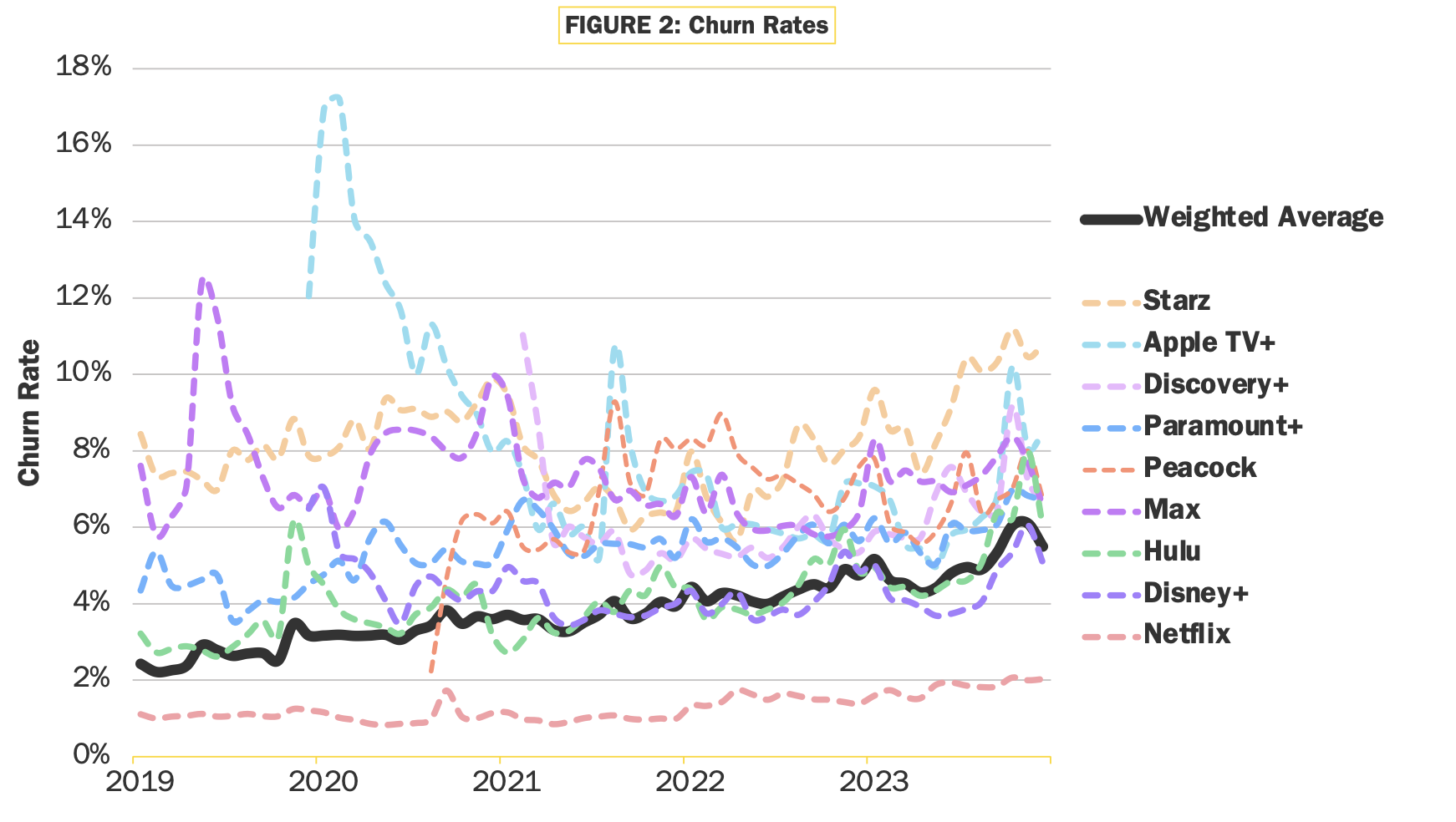

- The latest front in the war on churn: The Streaming Wars have officially morphed into the Churn Wars. Streaming adoption has slowed in the U.S., and now the truest test of success is customer retention. Not surprisingly, new data from Antenna shows that Netflix, the north star of streaming, has maintained the lowest churn rate by far, just over 2 percent at the end of 2023. This is about half the weighted average of the other premium services. It also suggests that Netflix has even more pricing power than analysts once thought.

On the other end of the spectrum, Starz (10.5 percent) and Apple TV+ (10 percent) have the highest churn rates. Meanwhile, Apple TV+ saw the highest percentage of re-subscribers (37 percent), which implies that Apple’s content investment strategy (including its MLS soccer package) may effectively be a marketing expense to win back those customers. This little wrinkle reveals one of the underappreciated complexities of this business: calculating (and re-calculating) the customer-acquisition cost and lifetime value of a subscriber, especially when they cancel and rejoin a service.

|

|

|

- Hollywood’s real A.I. threat: There was genuine alarm this week after OpenAI unveiled its latest miracle app: Sora, a generative A.I. tool that can turn text into convincingly realistic video. Fearing a job-killing apocalypse, Tyler Perry responded (allegedly) by putting his $800 million studio expansion on hold. But the freakout mostly misses the mark.

Yes, Hollywood will be cross-pressured by A.I. video tools, especially as they improve. (Compare Sora to, say, the first version of DALL-E, which OpenAI released in 2021, to see how quickly we’re moving toward A.I.-generated imagery that’s indistinguishable from the real thing.) But these are largely productivity enhancers, not job killers. Marvel gets raked over the coals by fans for even the most minor sins regarding its C.G.I.; studios aren’t going to outsource these functions to a bot when hundreds of millions of dollars are on the line.

Instead, as I’ve written here in the past, these A.I. tools are likely to have the biggest impact at the lower end of the quality spectrum. Sora wouldn’t have improved Zack Snyder’s Rebel Moon, but it could enable social video creators on platforms like YouTube or TikTok to make their own small-scale approximations of near-studio-quality video on a budget.

Remember, the most watched streaming service in the U.S. is actually YouTube, which commands nearly 10 percent of total video viewership, according to Nielsen. More than 500 million hours of content are uploaded every minute, and generative A.I. tools will make this content even better. It won’t be Hollywood level, at least not for a while, but it may be good enough… especially when YouTube is free.

|

|

| The Streamer Seven Year Itch |

| The first real signs of streaming consolidation are upon us. Five niche players, in particular, seem most vulnerable to the next wave. |

|

|

|

| Scan the homepage of your smart TV, and you’ll likely find apps for a dozen streaming services that no longer exist: MTV now redirects to Paramount+; HBO Go has been folded into Max; Funimation will shut down on April 2, and the Showtime app is set to be discontinued a few weeks later. There are other services that seem destined for obsolescence, too, like Warner Bros. Discovery’s B/R Sports add-on, which presumably will be sunsetted when the “Spulu” sports streaming bundle is unleashed, possibly this fall. And then there are the niche streamers (like Crunchyroll, Criterion Channel, or Sundance Now), some of which have found a strong base within a tiny market and some that don’t appear to have any economic justification for existing at all.

Prediction is a fool’s errand, yet here I find myself, time and time again. So instead of attempting to forecast when the most vulnerable streamers are likely to shutter, I’m going to explain why the end of each one is almost inevitable. Herewith, a chronicle of five streaming service deaths foretold… |

| 1. Bleacher Report Sports on Max |

|

| Let’s start with the most obvious. WBD’s unfortunately named B/R (Bleacher Report) Sports Add-On for Max always felt like C.E.O. David Zaslav’s desperate attempt to leverage sports rights to help prop up his streaming division. The total addressable market (TAM) for this product was always small: It didn’t satisfy local fans, casual fans, or die-hard fans.

Obviously, the B/R strategy makes even less sense now that WBD has teamed with Disney and Fox to create a skinny sports streaming bundle. Consequently, it’s hard to imagine any scenario in which the product continues beyond this year. While “Spulu” marks Fox’s only major foray into the direct-to-consumer market, and Disney has its much fuller ESPN D.T.C. app on the horizon, B/R Sports isn’t tailor-made for any specific customer set and could potentially cannibalize growth in the much more transparently valuable J.V. product. On WBD’s recent earnings call, Zaslav emphasized (yet again) that bundling is the future of streaming, and he expressed excitement about Spulu. He also admitted that B/R Sports was always anticipated to be a “wait-and-see,” stopgap product until something better came along.

Was that messaging shared internally? When B/R launched last fall, the plan was to begin charging subscribers an extra $9.99 a month beginning on March 1. Instead, the promotional period has been extended indefinitely as the executive team allegedly works through issues with its “tech integration.” Maybe they’d be better off pivoting toward Spulu now. |

|

|

| Speaking of stopgap services: Is there any future for the current iteration of ESPN+? The app carries a handful of sports, including MLB baseball, hockey, soccer, and exclusive UFC matches—but crucially, no NFL, thanks to contracts with cable carriers. ESPN+ boasts more than 25 million subscribers and an average revenue per user figure of $6.09 (up 14 percent year over year in the first quarter), but only a fraction of those are engaging with the app. Most simply bundled it in with Disney+ and Hulu. In fact, third-party firms estimate that ESPN+ has only 4 million to 6 million active users. According to Nielsen, less than 0.15 percent of all streaming viewing time in the U.S. was attributable to the service.

ESPN+ wouldn’t necessarily be made obsolete by the Spulu bundle, which will presumably be four or five times more expensive. But the current version of ESPN+ will likely become a lower tier of the new ESPN stand-alone streaming app that Disney C.E.O. Bob Iger has announced for 2025. This new, much ballyhooed service is expected to have all of the same content as the cable network, presumably at a price point somewhere in between the basic bundle and Spulu. If that sounds confusing, you’re not wrong. Consolidation is coming. |

|

|

| AMC+, the cable network’s streaming platform, leans more toward general interest audiences. But AMC Networks also owns smaller, niche services like Shudder (for horror fans) and Sundance Now (independent and documentary film). These services run anywhere from $6 to $7 a month compared to AMC+, which starts at $8.

So now, AMC is in this pickle where it has a subscale general interest streamer and three well-defined niche products. If Shudder or Sundance Now weren’t owned by AMC, I could see them operating into the future. Under one corporate umbrella, however, things look different—as many HBO executives know well. I suspect that AMC will eliminate the brand filters and bring all these entities together under AMC+, which will help with operating expenses and reduce the support needed to maintain a platform. Even then, maybe AMC+, with its 11 million-plus subscribers, will be on this list in a year or two anyway. |

|

|

| The writing is also on the wall for Freevee (formerly IMDb Freedive and IMDb TV), the free, ad-supported streaming service that comes with Amazon Prime. Like Fox-owned Tubi, another Gen Z favorite, Freevee’s model is based on capturing audiences that are seeking older catalog content and are unlikely to subscribe to paid services. But Freevee doesn’t generate big numbers for Amazon, and it potentially competes with Amazon Prime Video, which now includes advertising. (Prime members need to pay an additional $2.99/month to avoid them.)

Amazon reps have denied that Freevee, which is still available without a Prime membership, is shutting down. But it’s hard to envision it sticking around long term. For starters, Freevee is currently only available in three markets—the U.S., U.K., and Germany. Freevee also doesn’t make a dent in Nielsen’s monthly Gauge Report and, outside of Emmy nominee Jury Duty, hasn’t built out a strong audience. Engagement is key for FAST platforms, where the C.P.M. is defined by audience size and time spent. But the more people that use Freevee without Prime, the smaller the TAM for Amazon’s paid streaming service.

Could Freevee be rebranded as the cheapest, lowest tier of Prime Video? Seems likely. Perhaps its highest-value use case for Amazon is as a top-of-funnel marketing play in emerging regions like India, where the company is still developing its e-commerce business but looking for other ways to reach a large audience. |

|

|

| A quick reminder that Warner Bros. Discovery offers two fairly substantial streaming services: Max and Discovery+. The latter, introduced before Discovery merged with WarnerMedia, is dedicated to the cable series from platforms like Food Network, Investigation Discovery, and HGTV—you know, Guy Fieri, Chip & Joanna, and Dr. Pimple Popper. While most of its content is available on Max, Discovery+ is also available separately. (There is, of course, no Max content available on Discovery+).

Discovery+, which has the third-highest churn rate of all major S.V.O.D.s, at around 9 percent, and the lowest growth in share of subscriptions added in 2023 (3 percent), according to Antenna, is indeed confounding. Sure, there were more than 24 million subscribers as of April 2022 (WBD stopped breaking out individual numbers for Discovery+ and Max), but how many are still active? And how many of those subs would move to Max if the whole library was ported over?

Discovery+, on some level, encapsulates the latest trend. Larger media companies, which have had to defend their core businesses while entering streaming, are moving to a new phase—likely shuddering some early or ill-conceived ideas, while embracing new ones, even stopgaps like Spulu. Discovery+ and ESPN+ were always meant to be forums for experimentation and monetization while things played out. Now, these conglomerates are more informed and more disciplined than ever, and they need to streamline their focus. After all, none of them is guaranteed eternal life, either.

There’s one streamer conspicuously missing from this list: Paramount+. Paramount Global’s potential sale to David Ellison’s Skydance or Brian Roberts’ Comcast has turned Par+ into a product clouded in chaos. Reporting about what’ll happen changes so frequently that it’s difficult to know what anyone on the inside really wants to do, and even more difficult to make an educated guess about what could happen to Paramount+.

If it were up to me, and it is not, I’d find a way to merge the Paramount+ subscriber base with a service like Comcast’s Peacock, creating a strong sports and local news offering that can compete with Spulu and offer the biggest library catalog. The only issue is that if you’re Roberts, and you’re aware that Paramount Global may not be long for this world, why bid now when you can just wait for things to get even more dire? Somehow, however, I have a feeling we’ll still be talking about Paramount+ a year from now. |

|

|

|

| FOUR STORIES WE’RE TALKING ABOUT |

|

| R.F.K. Shrugged |

| An audit of Kennedy’s grueling audition for the Libertarian ticket. |

| PETER HAMBY |

|

|

| Cafe Milano |

| Show notes and deal chatter from the sidelines of Milan Fashion Week. |

| LAUREN SHERMAN |

|

|

| MLB’s Pantsgate |

| The stupid and increasingly serious micro-scandal defining baseball preseason. |

| JOHN OURAND |

|

|

| Spulu Agony |

| Could the D.O.J. kill the Disney-Fox-WBD sports streamer? |

| ERIQ GARDNER |

|

|

|

|

|

|

|

|

|

Need help? Review our FAQs

page or contact

us for assistance. For brand partnerships, email ads@puck.news.

|

|

You received this email because you signed up to receive emails from Puck, or as part of your Puck account associated with . To stop receiving this newsletter and/or manage all your email preferences, click here.

|

|

Puck is published by Heat Media LLC. 227 W 17th St New York, NY 10011.

|

|

|

|