|

|

Welcome back to What I’m Hearing+, live from Manhattan, where I just hosted a discussion with Alan Cumming about one of Peacock’s breakout hits, The Traitors. (If you missed it, we’ll have an article online soon.)

We’re in upfronts week, where eager television executives pitch new programming to vast rooms filled with ad buyers. In many ways, it’s the perfect backdrop to discuss the news that Warner Bros. Discovery and Disney are planning to bundle Max, Hulu, and Disney+. The announcement led to joking tweets and earnest LinkedIn posts about streaming becoming the “new cable.” I get the sentiment, but everything about this analogy is completely wrong.

But first…

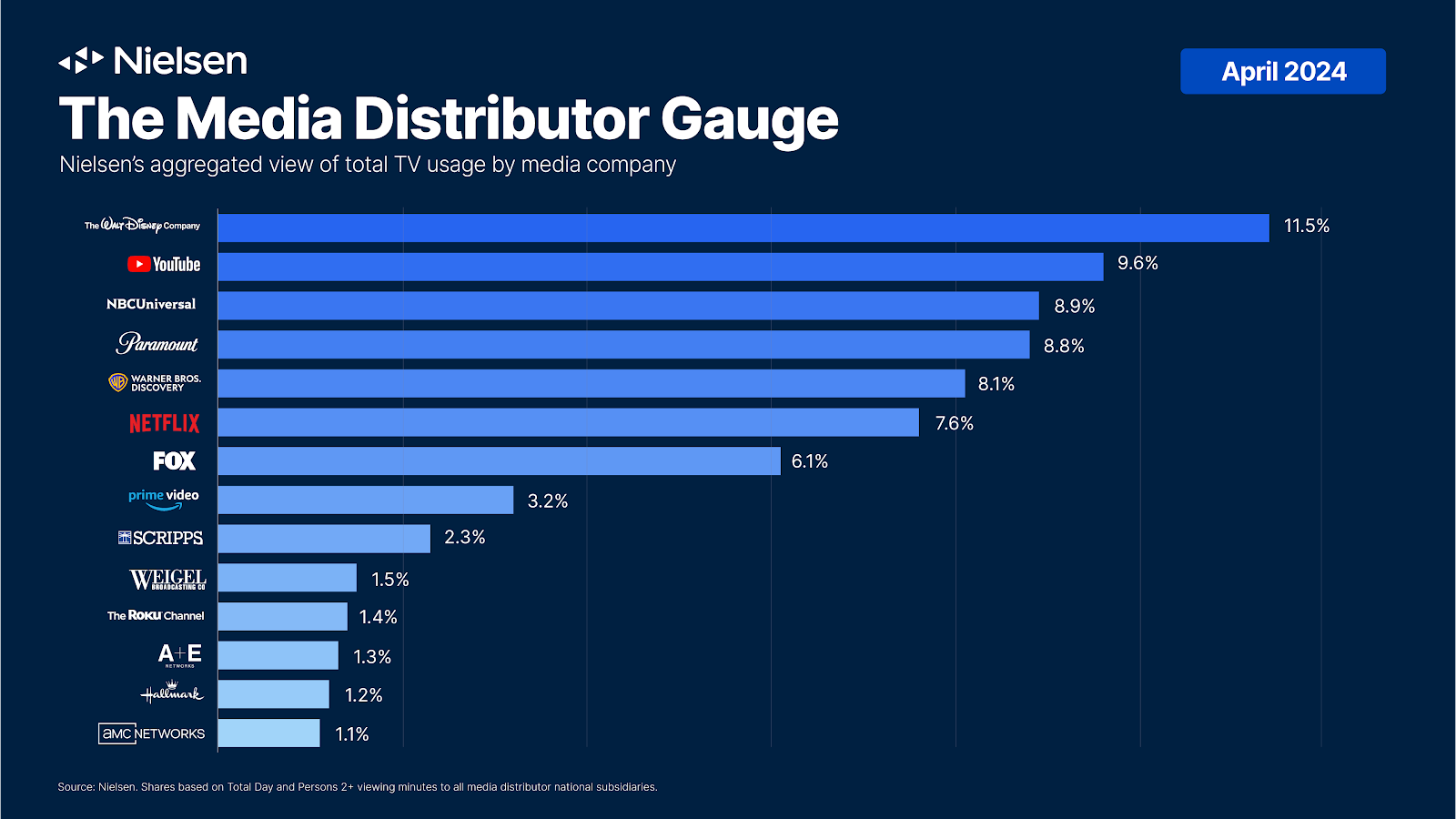

- Nielsen goes deeper: Today, Nielsen debuted a new “Media Distributor” gauge that effectively ranks all major media operators in the U.S. across streaming and linear (broadcast and cable). Disney, which accounted for 4.9 percent of all streaming viewership time in April—putting it in third place behind YouTube (9.6 percent) and Netflix (7.6 percent)—topped this list with an 11.5 percent share across all distribution formats. Netflix—which is only available via streaming, of course—fell to sixth place overall.

|

|

|

- A couple of quick takeaways here: First, sports matter. Fox sits above Prime Video in the ranking, commanding 6.1 percent of total viewership share. NBCUniversal is the third-strongest performer, with an 8.9 percent share, even though Peacock is the third-lowest performer on Nielsen’s streaming chart.

Second, this data doesn’t account for viewership on a given streamer via titles licensed from another company on the list. In other words, beloved CBS procedural NCIS, which streams on Netflix and often appears on Nielsen’s streaming top 10 list, counts toward Netflix’s total, not Paramount’s. So we’re still not getting the best picture of total attention by media operator, but it’s a much better look at the TV platform landscape as a whole.

And, finally, this data appears to confirm what sports leagues, politicians, and news organizations have been saying for years: broadcast is slowing, but it’s still a behemoth for viewership. Pay TV is another story, but companies like Disney, Paramount, NBCUniversal, and Fox still have a strong pitch to make at upfronts this week.

|

| And now to the main event… |

|

| The Disney+/Max Cable Fallacy |

| The new Bob Iger/David Zaslav streaming partnership has been compared, over and over again, to the halcyon days of the cable bundle. But those facile juxtapositions merely explain how little we really understand about the changes impacting the entertainment industry. |

|

|

|

| Several days ago, after the news broke that Warner Bros. Discovery’s Max and Disney’s own Disney+ and Hulu would be combined into a new streaming bundle, I received a fairly predictable joke text from a television executive that mirrored much of what I was reading online, particularly LinkedIn and X. “Cable redux,” this person said.

Yes, the pay TV business model was built on a collection of channels that were bundled into a single consumer product. And, yes, this corporate arrangement loosely approximates some version of that strategy. But this reductive theorizing about bundling completely ignores the key differences between the economics of streaming and pay TV.

When we talk about cable we are referring to a very specific incentive structure, a very specific unified product, and a very specific relationship between supplier and distributor. Pay TV bundling, after all, was traditionally a leverage game, in which the weakest channels in a seller’s package (like Freeform or truTV) rode on the coattails of the strongest (e.g., ESPN or TNT). For distributors, it was worth paying for a few dozen barely watched networks in order to secure the ones that subscribers couldn’t live without.

These days, however, the line between distributor and supplier has all but evaporated for most of the streaming juggernauts. And owning the relationship with a customer—having their viewing data, credit card information, geolocation, etcetera—is the coin of the realm. Rather than pursuing a singular focus on creating content and selling it to Charter, for example, WBD is concerned with interface technology, algorithmic recommendations, and editorial curation on homepages, all of which help the company utilize its shows and movies to attract and retain subscribers—and, over time, serve them ads.

Even if some of the same players are still around, the business incentives have changed dramatically from the halcyon days of cable. To wit: In the cable era, the original differentiator was scarcity—both the limited pathways to access video content and the small number of in-demand networks that consumers were willing to overpay for to watch their favorite shows. Streaming widened the aperture by multiplying the number of pathways and flooding the marketplace with content, which made it all seem more indistinguishable. Cable companies were stable and static businesses, whereas streamers must constantly worry about month-over-month churn.

One of the collective delusions among legacy media companies, especially in the early days of the streaming wars, was the notion that their content was so differentiated, so special, that customers would search across multiple streamers to find it. As we’ve discovered, however, that’s just not the case. People don’t peruse streaming like they did old-school television. And they’ve also been proven to be more price-sensitive, perhaps wary of the way cable companies gouged them for years. In 2022, Deloitte estimated the average number of streamers per household at four. In 2023, a Forbes study estimated it was down to three.

So, no, this isn’t cable redux. But an examination of the profound and often latent differences between the two economic ecosystems might illuminate not only the reasoning behind the deal between David Zaslav and Bob Iger, but why it might work. |

|

|

| I often think about the streaming industry in terms of SKUs, or stock keeping units, the very academic industrial term used to manage inventory products. Warner Bros. Discovery has three streaming SKUs: Max, Discovery+, and this new combined offering. Spulu, once it graces us, will be a fourth focused on sports. Disney currently has multiple SKUs domestically—Disney+, ESPN+, Hulu, Hulu With Live TV, this new deal, the future Spulu, and more.

But Disney, Max, and even Paramount+ (with its Showtime bundle) have started slimming down their offerings into one (or one-ish) unified product. On the one hand, this limits near-term revenue opportunities by depriving customers of options. On the other, it is an attempt to improve the customer experience and increase the lifetime value of each user by showcasing more content in a single place—similar to the strategy employed by not only Netflix (one SKU) but, yes, cable. Jim Barksdale, the Netscape visionary and longtime tech executive, neatly summarized the history of the media business when he said, “There’s only two ways I know of to make money—bundling and unbundling.”

Cable companies, for their part, created one product out of multiple networks, which became a veritable utility for middle-class homes, on par with the water or electric bill, and it was an enormously profitable. These days, however, cable service hasn’t been replaced by WBD-Disney partnerships but something far more formidable: the massive technology companies competing to mediate, and collect rent on, the relationship between consumers and their entertainment needs.

Apple, Amazon, Google, and Roku, among other intermediaries, have invested billions of dollars in their efforts to control the end-to-end user journey. Apple’s App Store takes 15 to 30 percent of all subscription fees, which is one reason why you can’t sign up for Netflix through the App Store. Amazon takes about a similar percentage of subscription fees as well when you sign up through their Fire TV platform. Furthermore, companies like Amazon and Roku take advertising inventory.

To continue the Barksdale philosophizing, the history of the media industry does indeed often come down to the oscillations between bundling and unbundling. The rise of Netflix in the aughts forced all the biggest players to build walls around their gardens and bundle their products together. Then, two years ago, the Great Netflix Correction led to a collective about-face in the marketplace: After racking up billions in debt trying to build their own Netflix killers, competing executives started to prioritize cashflow above subscriber goals and began unbundling—licensing their shows to other platforms in return for steady revenue.

Now, we’re now seeing a new kind of rebundling. Not only are WBD and Disney partners in this newly announced venture, they also have the aforementioned Spulu in the works with Fox. This week, Comcast C.E.O. Brian Roberts announced a Peacock-Netflix-Apple TV+ bundle for Comcast broadband and TV customers. Media, it seems, has officially entered a new frenemies stage. So long as there are opportunities, however, for a mass consumer base to access mass media through a myriad of distribution options, “the new cable” can’t exist.

These partnerships work best when their signatories’ needs truly complement one another. In the Max-Hulu-D+ arrangement, the quid pro quo seems pretty simple. Disney has a strong need for access to customer data across its medley of businesses, and the sports assets and supplementary sports tools (betting) to create a one-touchpoint ecosystem. And WBD needs to pay down tens of billions in debt just to attempt a debt re-rating.

Meanwhile, bundling streamers has been shown to reduce churn, which is increasingly a problem across all major services, besides Netflix, in the U.S. Bundling can also theoretically increase scale while establishing a much higher lifetime-value-to-customer-acquisition-cost (LTV-CAC) ratio, which is the lifeblood of a subscription service. After all, compared to Apple, Amazon, and Google, all these companies need each other.

And that may suggest the ultimate differentiator between cable and this new wave of streaming partnerships. In many ways, the pay TV model was one of the most robust in recent economic history. And its solidity made it reliable, predictable, and unchanged. Despite the extraordinary adoption curves, we’re still in the early days of streaming—a model that was built on experimentation and strange bedfellows (all that bundling and unbundling), and that’s not going away anytime soon. |

|

|

|

| FOUR STORIES WE’RE TALKING ABOUT |

|

|

|

|

|

| Pleading the 6th |

| A bracing chat with the filmmakers behind ‘The Sixth.’ |

| PETER HAMBY |

|

|

|

|

|

|

|

|

|

|

|

Need help? Review our FAQs

page or contact

us for assistance. For brand partnerships, email ads@puck.news.

|

|

You received this email because you signed up to receive emails from Puck, or as part of your Puck account associated with . To stop receiving this newsletter and/or manage all your email preferences, click here.

|

|

Puck is published by Heat Media LLC. 227 W 17th St New York, NY 10011.

|

|

|

|